(With Calculators) Budgeting & Retirement Rules That You Should Know In 2026

Budgeting & Retirement Rules | Representative Image

If you want to properly manage your money in 2026, then just increasing your income is not enough. In today’s time as our conuntry is growing the inflation is also going high. The rent and daily expenses are increasing very fast, and job security is also not stable anymore. Because of this, traditional budgeting rules like 50/30/20 do not feel practical for everyone now, especially in metro cities where needs go above 50%.

But the good thing is that financial planning is still simple if you use rules in a flexible way. These rules are not rigid. They are just starting points. You have to adjust them based on your lifestyle and income.

In this article, you will get 7 powerful budgeting and retirement rules that work in real life. Along with that, you will also get simple calculators so you can instantly calculate your budget, savings, and retirement planning.

All this content is explained in easy language so even beginners can understand it and apply it immediately.

Key Takeaways On Budgeting & Retirement Rules

- 50/30/20 rule is a strong starting point for beginners but it needs flexibility

- 70/20/10 rule is very useful in high expense and debt situations

- Emergency fund should be at least 6 months in 2026 for safety

- 24 hour rule is the best habit to control impulse spending

- For retirement, understanding 25x and 4% rule is very important

50/30/20 Rule: Simple But Powerful Budgeting Formula

The 50/30/20 rule is the most popular budgeting method. This rule is simple and beginner friendly. It divides your income into three categories.

->50% of income goes to needs. This includes rent, groceries, electricity, and transport.

->30% of income goes to wants. This includes entertainment, shopping, and dining out.

->20% of income goes to savings and investments.

Example: If your monthly income is ₹50,000:

₹25,000 for needs

₹15,000 for wants

₹10,000 for savings

Calculator:

Income × 20% = Monthly Savings

But in 2026, the problem is that needs have increased a lot. Many people cannot manage needs within 50%. So you can adjust it.

Example modified version:

->40% needs

->30% wants

-> 30% savings

The important thing is that your saving habit should not break.

Benefits:

- Simple and easy to follow

- Balances lifestyle and savings

- Controls overspending

- Best for beginners

One smart tip is “pay yourself first”. Save money as soon as salary comes and then spend.

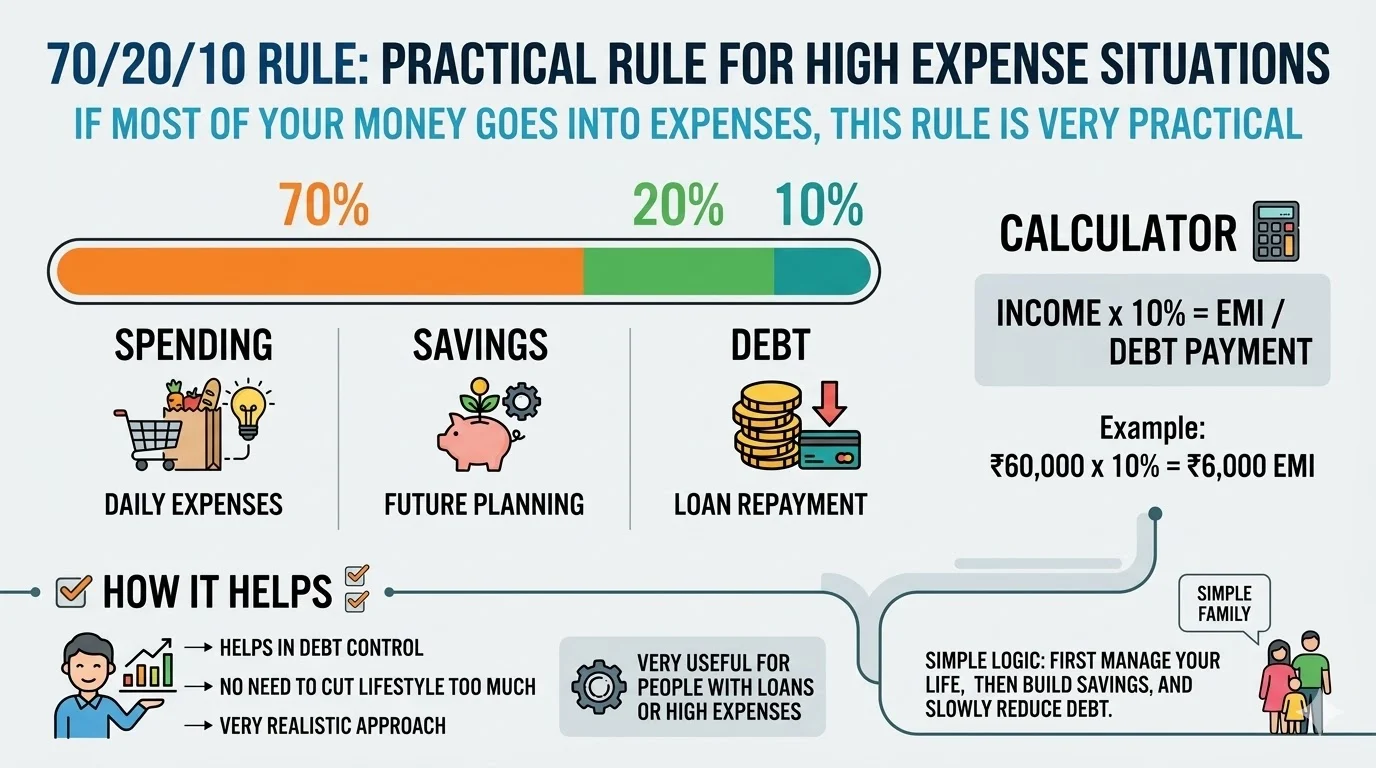

70/20/10 Rule: Practical Rule for High Expense Situations

If most of your money goes into expenses, then this rule is very practical.

| Category | Percentage | Use |

|---|---|---|

| Spending | 70% | Daily expenses |

| Savings | 20% | Future planning |

| Debt | 10% | Loan repayment |

Calculator:

Income × 10% = EMI / Debt Payment

Example:

₹60,000 × 10% = ₹6,000 EMI

This rule is useful for people who have loans or high expenses.

How it helps:

- Helps in debt control

- No need to cut lifestyle too much

- Very realistic approach

The logic is simple. First manage your life, then build savings, and slowly reduce debt.

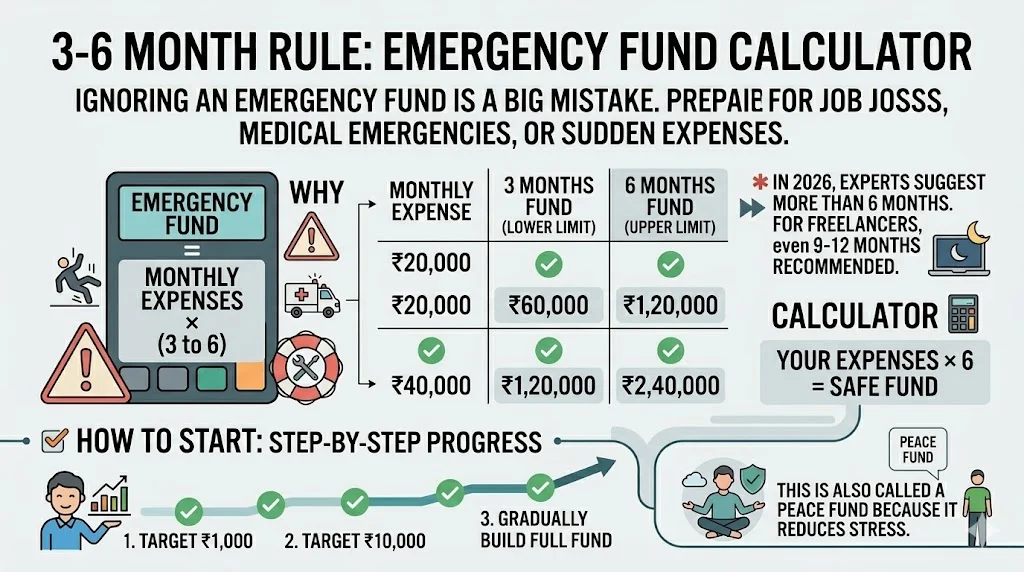

3-6 Month Rule: Emergency Fund Calculator

Ignoring an emergency fund is a big mistake. Job loss, medical emergency, or sudden expense can happen anytime.

Formula:

Monthly Expenses × 3 to 6

| Monthly Expense | 3 Months Fund | 6 Months Fund |

|---|---|---|

| ₹20,000 | ₹60,000 | ₹1,20,000 |

| ₹40,000 | ₹1,20,000 | ₹2,40,000 |

Calculator:

Expenses × 6 = Safe Fund

In 2026, experts suggest more than 6 months. For freelancers, even 9 to 12 months is recommended.

How to start:

- First target ₹1,000

- Then ₹10,000

- Gradually build full fund

This is also called a peace fund because it reduces stress.

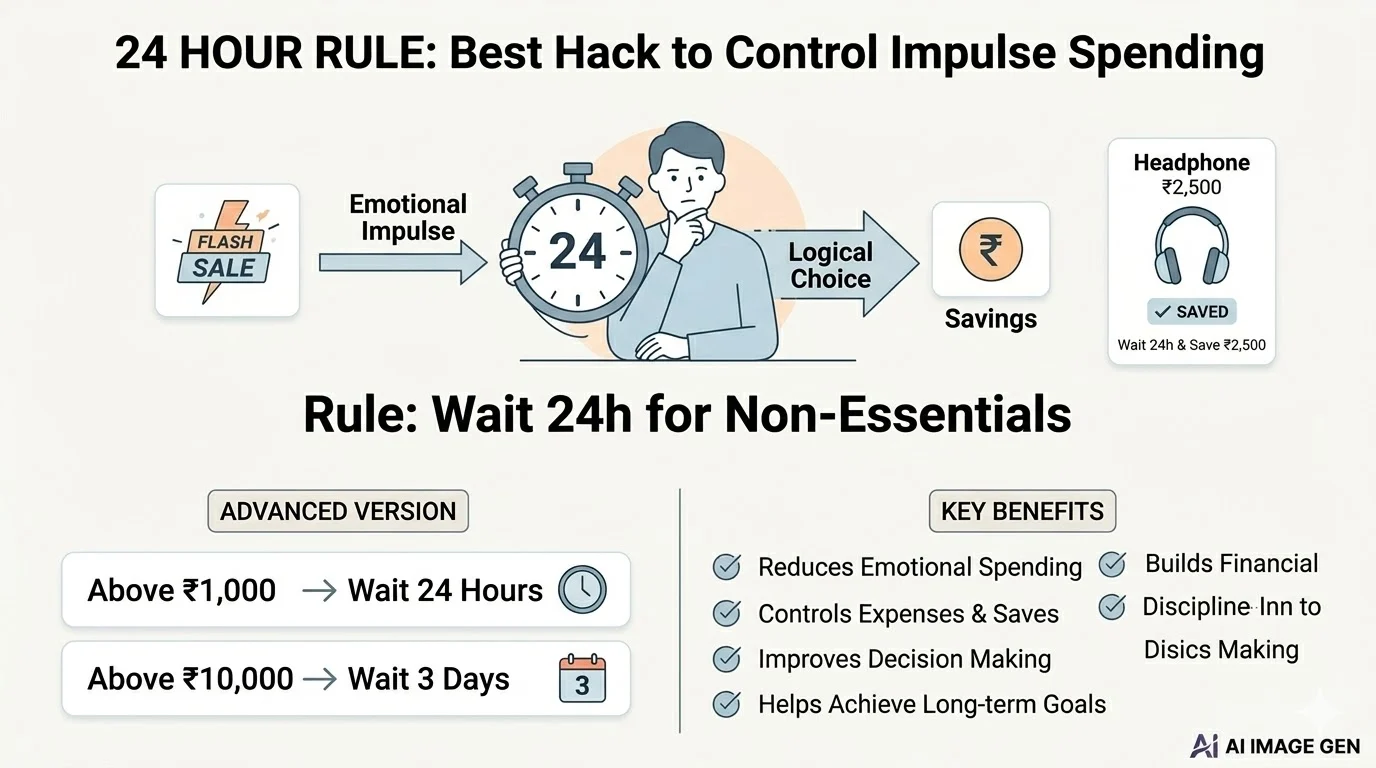

24 Hour Rule: Best Hack to Control Impulse Spending

The 24 hour rule is a simple but highly effective tool to control unnecessary spending. In today’s digital world, online ads, flash sales, and instant payments make people buy impulsively. This rule protects you from emotional spending.

Rule:

If you want to buy a non essential product, do not buy immediately. Wait at least 24 hours and then decide.

How it works:

This rule gives you time to come out of emotional excitement and take a logical decision. In most cases, after 24 hours you realize that the purchase is not necessary.

Example:

You see a headphone worth ₹2,500 online and feel like buying it instantly. But you follow the 24 hour rule. The next day, you realize you already have a working headphone. Result: you save ₹2,500.

Advanced Version:

- Above ₹1,000 → wait 24 hours

- Above ₹10,000 → wait 3 days

Benefits:

- Reduces impulse buying

- Controls unnecessary expenses

- Increases savings automatically

- Builds financial discipline

- Improves decision making

- Reduces emotional spending

- Helps achieve long term goals

In 2026, where spending is very easy, following this rule is very important. It is a small habit but can completely change your financial life.

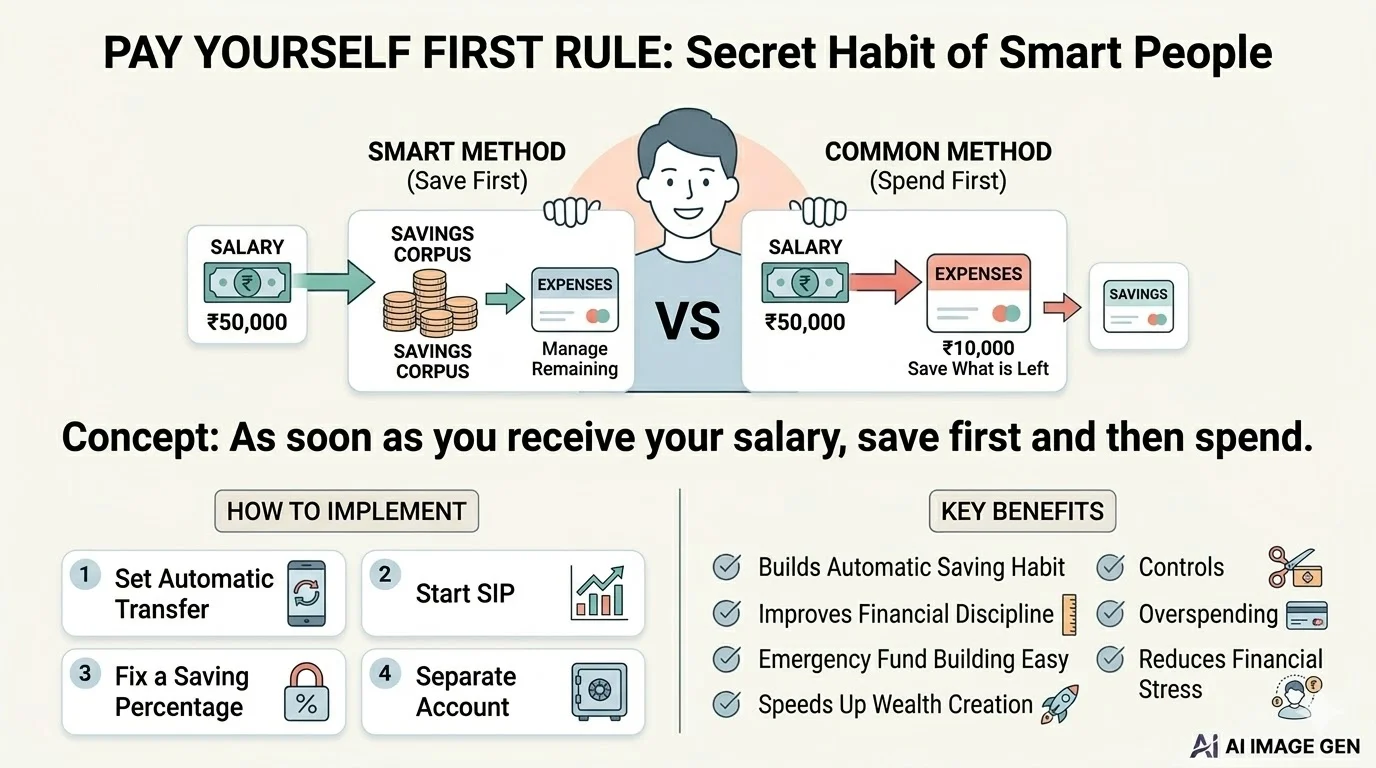

Pay Yourself First Rule: Secret Habit of Smart People

This rule is simple but very effective and important for smart financial planning in 2026. It is called “Pay Yourself First” because you save for your future first and then manage expenses.

Most people do the opposite. They spend first and save what is left. But in this method, saving becomes the priority.

Concept:

As soon as you receive your salary, save first and then spend. You transfer a fixed percentage of your income into savings, and manage expenses with the remaining amount.

Example:

Monthly income ₹50,000

20% saving = ₹10,000

Remaining ₹40,000 for expenses

This method builds automatic saving habit and over time creates a big corpus.

How to implement:

- Set automatic bank transfer for savings

- Start SIP so money gets invested automatically

- Fix a saving percentage and follow strictly

- Keep a separate savings account

Benefits:

- Builds automatic saving habit

- Improves financial discipline

- Makes emergency fund building easy

- Speeds up wealth creation

- Controls overspending

- Reduces financial stress

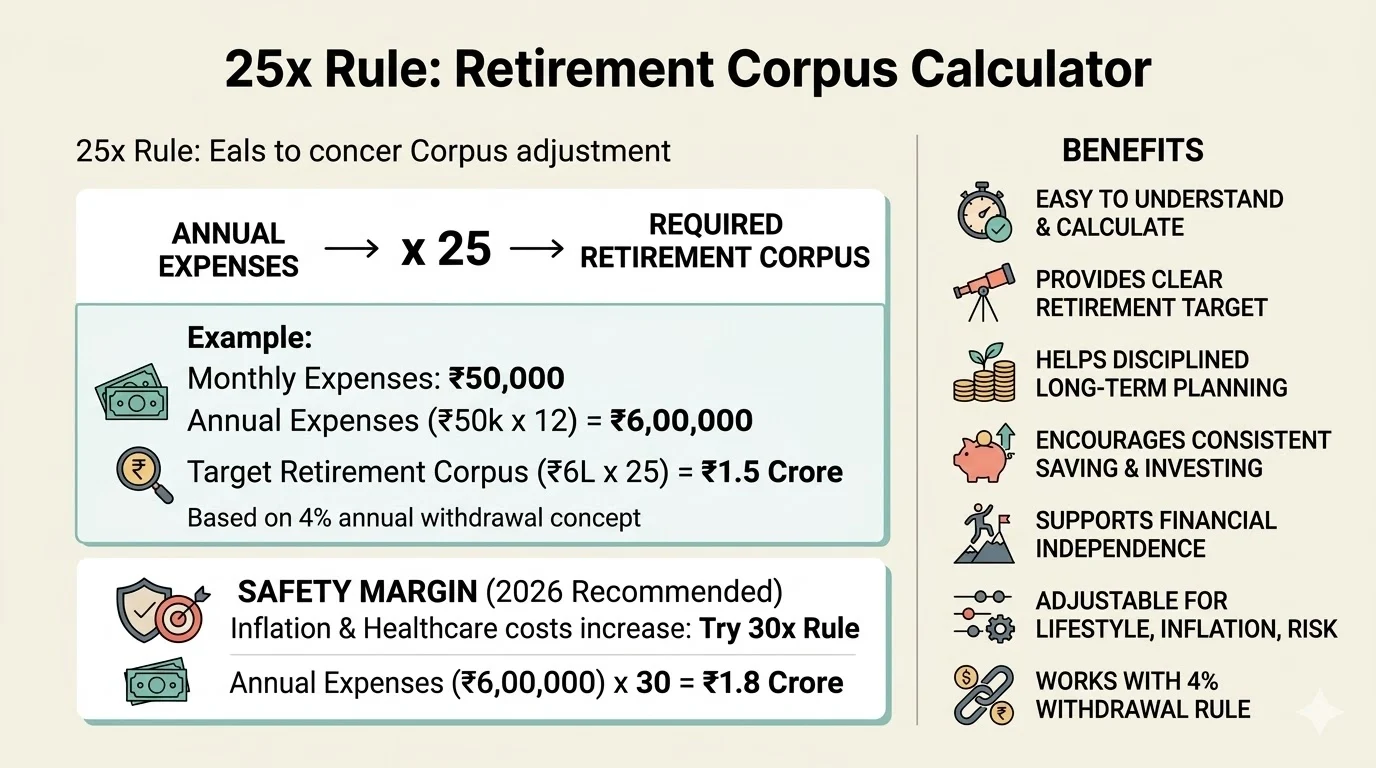

25x Rule: Retirement Corpus Calculator

The 25x rule is a simple yet powerful retirement planning tool that helps you estimate how much money you need to retire comfortably. The idea behind this rule is that if you accumulate a corpus equal to 25 times your annual expenses, you can sustain your lifestyle without running out of money. It is based on the concept that you can withdraw around 4% of your total savings every year while the remaining amount continues to grow through investments.

Formula:

Annual Expenses × 25

This means you first calculate your yearly expenses and then multiply that number by 25 to get your target retirement corpus.

Example:

Let’s say your monthly expenses are ₹50,000.

Annual expenses = ₹50,000 × 12 = ₹6,00,000

Required retirement corpus = ₹6,00,000 × 25 = ₹1.5 Crore

So, if you build a corpus of ₹1.5 crore, you can withdraw approximately ₹6,00,000 per year (4%) to cover your expenses. However, due to rising inflation and increasing healthcare costs in 2026, many experts recommend using a safer multiple like 30x. In this case, your target corpus would be ₹6,00,000 × 30 = ₹1.8 Crore, giving you a better safety margin.

This rule is especially useful because it gives you a clear and realistic financial goal. Instead of guessing how much you need, you can plan your savings and investments accordingly.

Benefits:

- Easy to understand and calculate, even for beginners

- Provides a clear retirement target, reducing confusion

- Helps in disciplined long-term financial planning

- Encourages consistent saving and investing habits

- Supports financial independence by setting a defined goal

- Can be adjusted based on lifestyle, inflation, and risk tolerance

- Works well with other strategies like the 4% withdrawal rule

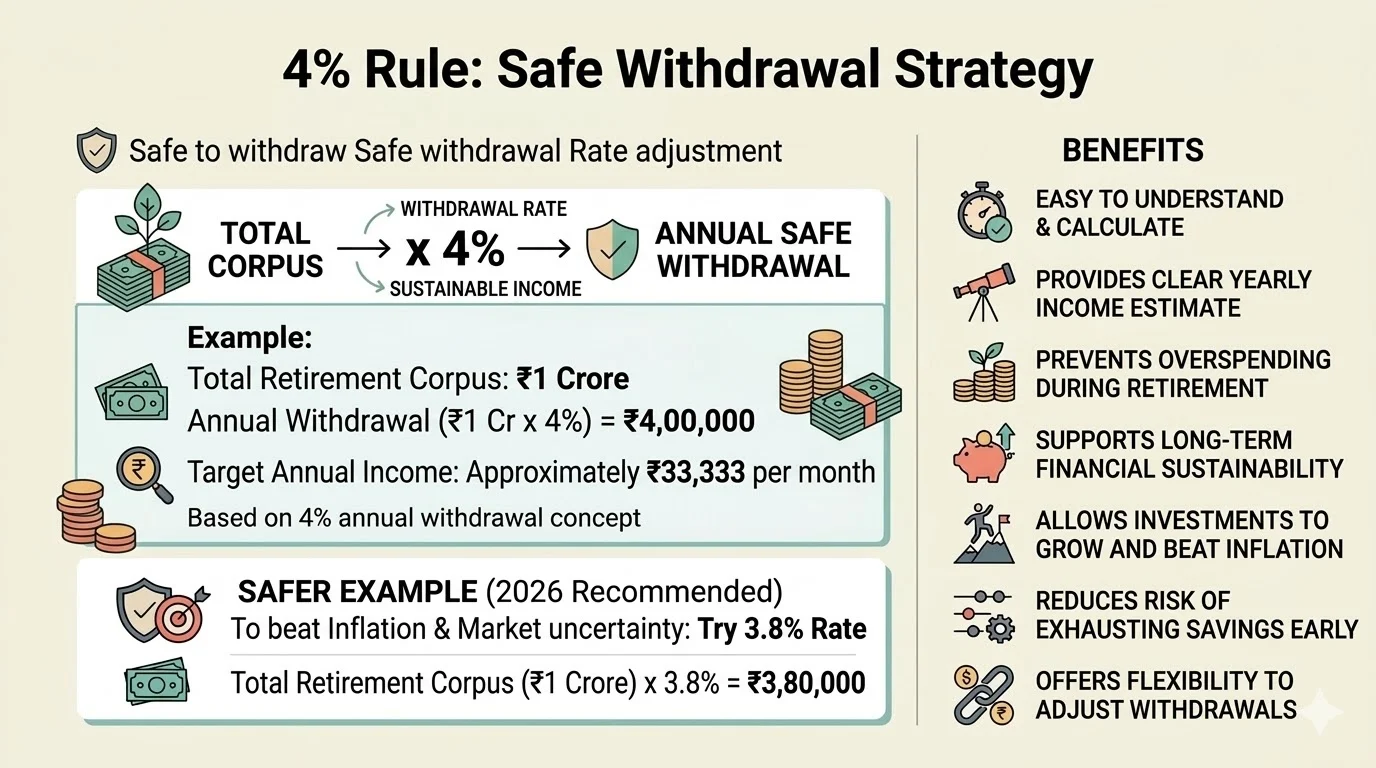

4% Rule: Safe Withdrawal Strategy

The 4% rule is a widely used retirement planning tool that helps you decide how much money you can safely withdraw from your retirement corpus every year without running out of funds too early. The idea behind this rule is to maintain a balance between withdrawing money for your expenses and allowing the remaining amount to stay invested so it can continue to grow over time.

Use Tool: 4% Retirement Rule Calculator

Formula: Total Corpus × Withdrawal Rate

This rule suggests that you can withdraw 4% of your total retirement savings annually. The remaining amount stays invested, which helps your money grow and keeps up with inflation.

Example: If your total retirement corpus is ₹1 Crore, then:

₹1,00,00,000 × 4% = ₹4,00,000 per year (approximately ₹33,333 per month)

However, due to rising inflation and market uncertainty in 2026, experts recommend a slightly safer withdrawal rate of 3.7% to 3.9%.

Safer Example: ₹1 Crore × 3.8% = ₹3,80,000 per year

This lower withdrawal rate ensures that your money lasts longer and reduces the risk of running out of funds during retirement.

The 4% rule works best when your investments are diversified across assets like equity, debt, and other instruments that can generate stable returns over time.

Benefits of the 4% Rule:

- Simple and easy to understand, even for beginners

- Provides a clear estimate of yearly retirement income

- Helps prevent overspending during retirement

- Supports long-term financial sustainability

- Allows your investments to grow and beat inflation

- Reduces the risk of exhausting your savings too early

- Offers flexibility to adjust withdrawals based on market conditions

Overall, the 4% rule gives you a practical starting point for planning your retirement income and helps you maintain financial stability throughout your retirement years.

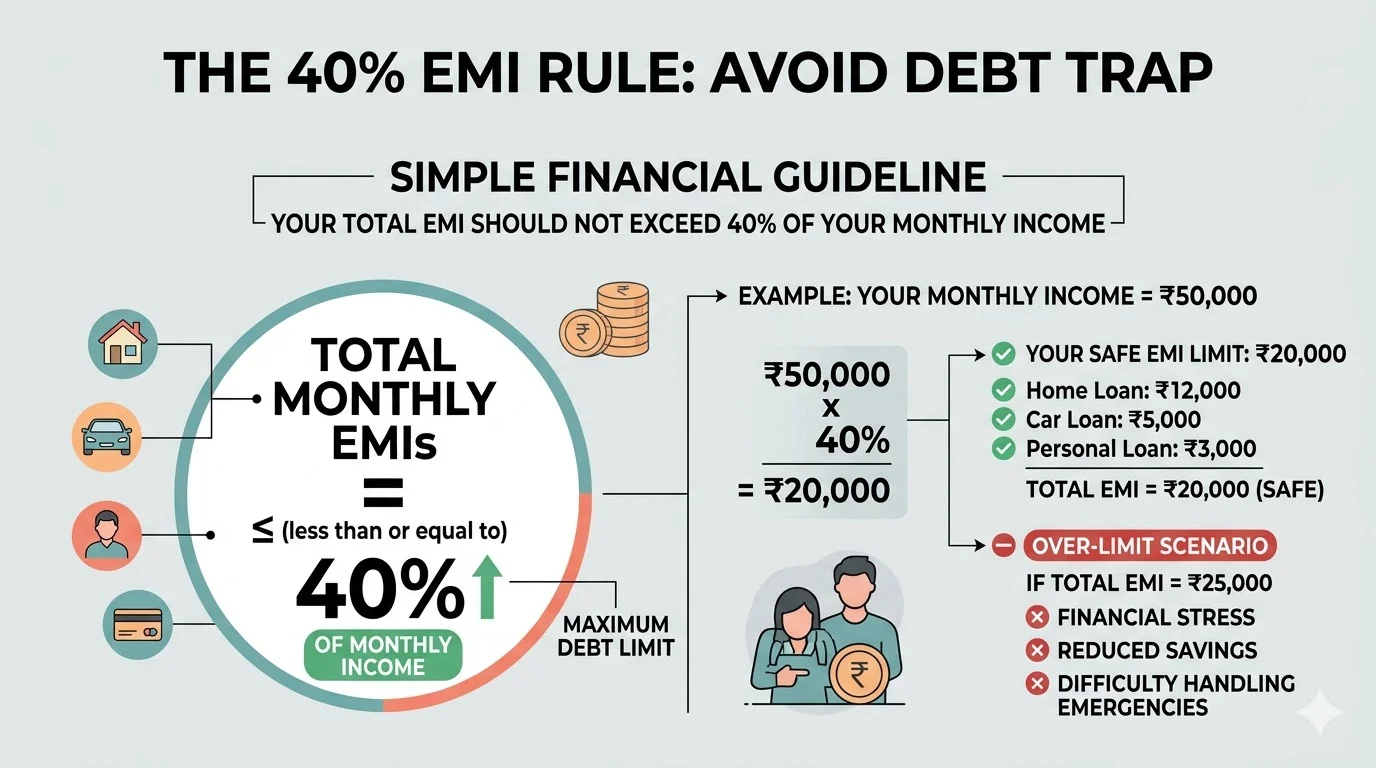

40% EMI Rule: Formula to Avoid Debt Trap

The 40% EMI rule is a simple but powerful guideline that helps you manage your loans without putting too much pressure on your finances. According to this rule, your total EMI (Equated Monthly Installment), including home loan, car loan, personal loan, and credit card EMIs, should not exceed 40% of your monthly income.

The main purpose of this rule is to ensure that you have enough money left for your daily expenses, savings, and emergencies. If a large portion of your income goes into EMIs, it becomes difficult to manage your lifestyle and financial goals.

Example:

Suppose your monthly income is ₹50,000.

According to the 40% rule:

₹50,000 × 40% = ₹20,000

This means your total EMI should not go beyond ₹20,000. For instance, if you are paying ₹12,000 for a home loan, ₹5,000 for a car loan, and ₹3,000 for a personal loan, your total EMI becomes ₹20,000, which is within the safe limit.

However, if your EMI increases to ₹25,000, it will exceed the recommended limit. This can lead to financial stress, reduced savings, and difficulty in handling unexpected expenses.

This rule is especially useful when you are planning to take a new loan. Even if banks approve a higher loan amount, you should always check whether it fits within your 40% EMI limit.

Benefits of the 40% EMI Rule:

- Helps maintain a healthy balance between income and expenses

- Reduces financial stress and anxiety

- Ensures you have enough money for savings and investments

- Provides flexibility to handle emergencies

- Prevents over borrowing and debt traps

- Supports long-term financial stability

- Improves overall money management discipline

Following this rule can help you stay financially secure while still enjoying your lifestyle without unnecessary pressure.

How To Applay These Rules In Real Life

Understanding theory is easy but applying it is important.

Step by Step:

- Track expenses for 1 to 2 months

- Divide into categories

- Choose one rule

- Implement slowly

Tools:

- Use Excel sheet

- Use budgeting apps

- Set automatic transfers

Common mistakes:

- Ignoring lifestyle inflation

- Not building emergency fund

- Over investing without plan

Comparison: Which Rule to Use

| Rule | Best For | 2026 Adjustment |

|---|---|---|

| 50/30/20 | Beginners | Flexible percentages |

| 70/20/10 | High expenses | Debt focus |

| Emergency Fund | Everyone | 6+ months |

| 24 Hour Rule | Overspenders | Longer wait |

| 25x Rule | Retirement | 25-30x |

| 4% Rule | Withdrawal | 3.7-3.9% |

Which Rule Is Best For You

- If you are a beginner → start with 50/30/20

- If expenses are high → try 70/20/10

- If job is unstable → build emergency fund

- If overspending → follow 24 hour rule

- For retirement → use 25x and 4% rule

My Final Thoughts On Budgeting Rules

The truth is, no budgeting rule is perfect, and honestly, it doesn’t have to be. These are just guidelines to help you get started. In 2026, the smartest people are not the ones who follow rules blindly, but the ones who understand their own situation and adjust accordingly.

If I had to give you one simple piece of advice, it would be this don’t try to follow everything at once. Just pick one rule that feels right for you and start there. Stay consistent with it. Over time, you’ll naturally understand what works for you and what doesn’t, and slowly you’ll build your own system that fits your life.

At the end of the day, financial planning is not as complicated as it looks. It’s more about small habits, patience, and staying consistent. If you can do that, you’re already ahead of most people, and you’ll be able to build a strong and secure financial future for yourself.

Related Posts :

Share This Post