[With Calculators] Investing & Loan Rules That You Should Know In 2026

![[With Calculators] Investing & Loan Rules That You Should Know In 2026 | Representative Image](https://sktak.in/wp-content/uploads/2026/03/With-Calculators-Investing-Loan-Rules-That-You-Should-Know-In.webp)

[With Calculators] Investing & Loan Rules That You Should Know In 2026 | Representative Image

Managing money in 2026 feels more confusing than ever. Expenses are rising as we are living in developing nation. EMIs are increasing. Investment options are growing but clarity is missing.

Many people feel stuck between saving, investing, and paying off loans. This is where simple money rules become useful. These rules are not perfect formulas. They are easy mental shortcuts that help you take better decisions without stress.

Most people read about these rules but do not know how to apply them in real life. That is the real problem. In this guide, you will learn both investing rules and loan rules in a practical way. You will see how to use them with real examples. You will also understand where these rules fail and how to adjust them for 2026 conditions in India.

If you are earning a salary, paying EMIs, or starting your financial journey, this guide will help you build clarity. The goal is simple. Help you manage money better with less confusion and more confidence. In this blog post you will get different types of proven rules related to any type of loan & invetement. Read this highly informative posts. I Promise to you that you will not regret your next 10 minutes

Table of Contents

Key Takeaways On Investing & Loan Rules

- Simple money rules help you take fast and better financial decisions

- Rule of 72 and 114 show how compounding builds wealth over time

- Asset allocation rules must adjust for longer life and inflation

- EMI and debt rules protect your cash flow and reduce stress

- Combining investing and debt rules works better than following one rule

Why Simple Money Rules Matter More In 2026

In 2026, financial life has changed a lot. Inflation is higher than before. Living costs are rising. Loans are easily available. Many people take loans without planning. At the same time, investing options have increased. Mutual funds, stocks, and digital platforms are everywhere.

Because of this, people face decision fatigue. Too many options create confusion. This is why simple rules help. They reduce thinking time. They give direction. They help you stay disciplined. These rules are not perfect. But they help you avoid big mistakes. That is their real value.

Use Tool: 28/36 Rule Calculator

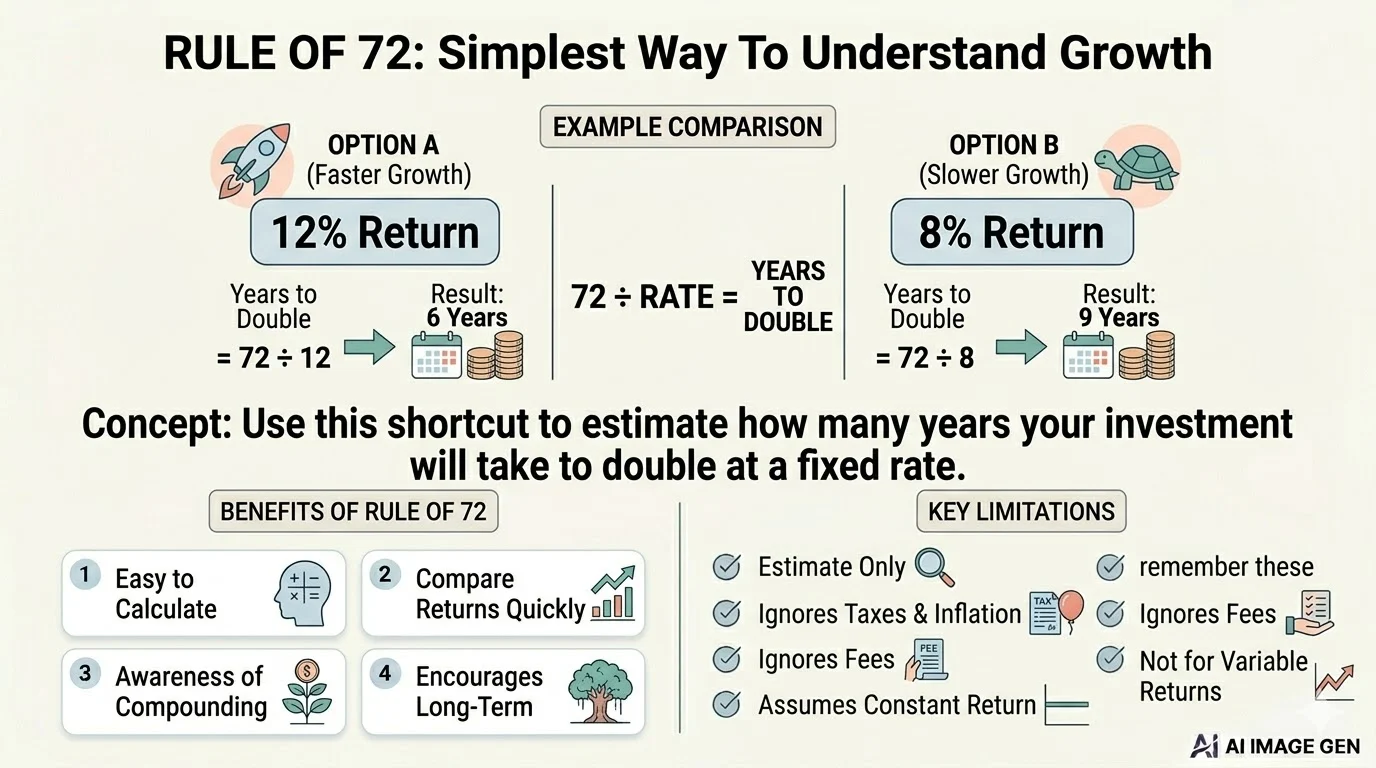

Rule Of 72: The Simplest Way To Understand Growth

Rule of 72 is a simple and powerful tool that helps you understand how quickly your money can grow through compounding. It gives you a quick estimate of how many years it will take for your investment to double at a fixed rate of return. Instead of using complex formulas, you can use this shortcut to make faster financial decisions.

Formula: Years to double = 72 divided by annual return rate

For example, if your investment earns 12 percent per year, you divide 72 by 12. The result is 6. This means your money will double in approximately 6 years. If the return is 8 percent, then 72 divided by 8 equals 9 years. So, your money will take around 9 years to double.

This rule is especially useful when comparing different investment options. For instance, if one investment offers 10 percent return and another offers 6 percent, you can quickly see that the first option will double your money faster. It also helps you understand the long-term impact of compounding, encouraging you to stay invested for a longer period.

Benefits of Rule of 72:

- Easy to calculate without a calculator

- Helps compare different investment returns quickly

- Builds awareness about the power of compounding

- Encourages long-term investing mindset

- Useful for both beginners and experienced investors

However, it is important to remember that this rule provides only an estimate. It does not consider taxes, inflation, or investment fees. It also assumes a constant rate of return, which is not always realistic in market-based investments. Despite these limitations, the Rule of 72 remains a practical and widely used tool for making smarter financial decisions.

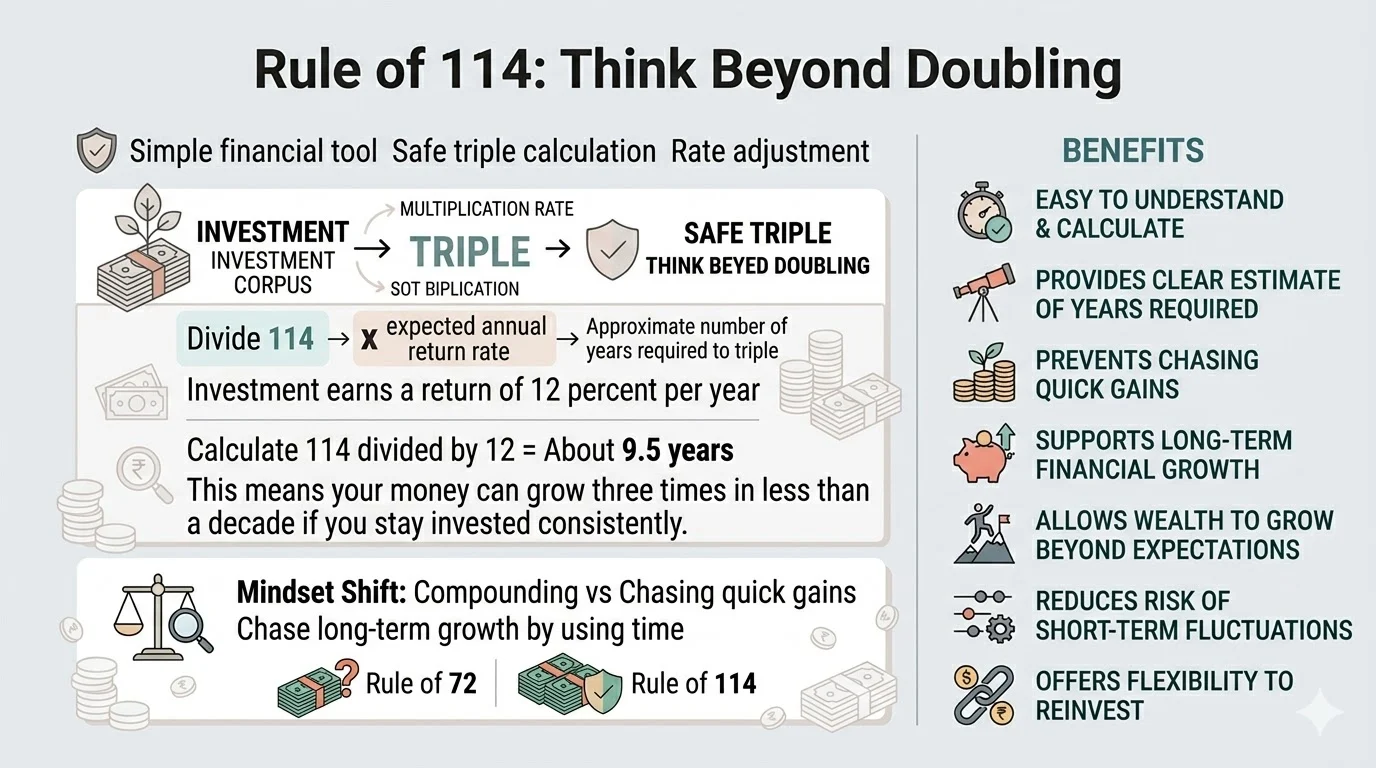

Rule Of 114: Think Beyond Doubling

Most people only think about doubling money. But real wealth comes from long term growth, and that is where the Rule of 114 becomes useful. This simple financial tool helps you estimate how long it will take for your investment to triple in value. It works in a similar way to the Rule of 72, but instead of focusing on doubling, it shifts your thinking toward bigger, long-term goals.

The formula is straightforward. You divide 114 by your expected annual return rate. The result gives you the approximate number of years required to triple your investment.

For example, if your investment earns a return of 12 percent per year, you calculate 114 divided by 12, which equals about 9.5 years. This means your money can grow three times in less than a decade if you stay invested consistently.

This rule is powerful because it changes your mindset. Instead of chasing quick gains, you begin to understand the value of patience and compounding. Over 15 to 20 years, your wealth can grow far beyond expectations, especially when returns are reinvested.

Benefits of using the Rule of 114:

- Helps you set long-term financial goals with clarity

- Makes it easier to compare different investment options

- Encourages disciplined and consistent investing

- Simplifies complex compounding calculations

- Builds patience by showing the power of time in wealth creation

By using this rule, you can make smarter investment decisions and stay focused on long-term growth rather than short-term fluctuations.

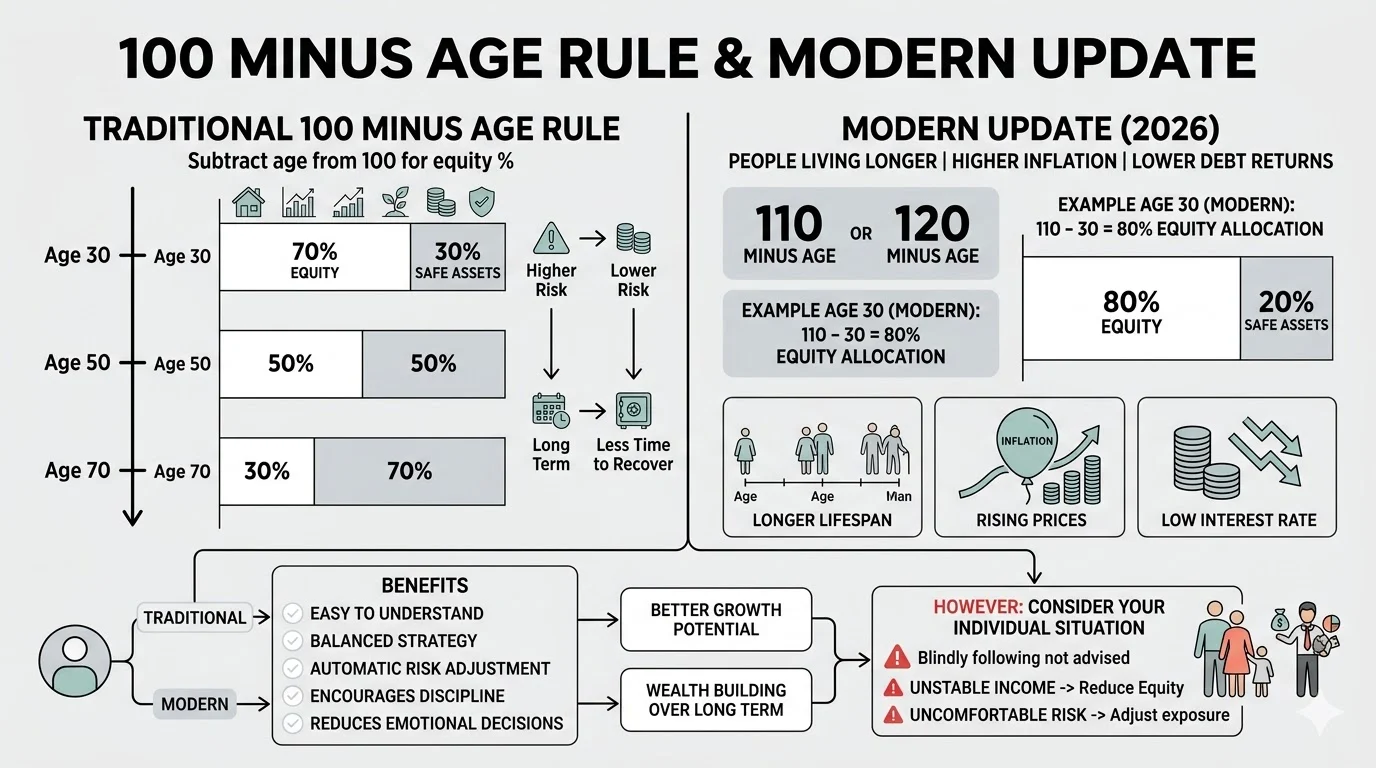

100 Minus Age Rule And Modern Update

The 100 minus age rule is a simple tool used to decide how much of your investment should go into equity, such as stocks or equity mutual funds. The idea behind this rule is to balance risk and safety based on your age. Younger investors can take more risk because they have more time to recover from market fluctuations, while older investors should focus more on stability.

The formula is straightforward. You subtract your age from 100 to get the percentage of your portfolio that should be invested in equity. The remaining amount can be invested in safer options like debt funds or fixed deposits.

For example, if you are 30 years old, you subtract 30 from 100. This means 70 percent of your investments can be in equity, and the remaining 30 percent can be in safer assets. This approach helps you maintain a balanced portfolio that grows over time while managing risk.

However, in 2026, this rule is evolving. People are living longer, inflation is higher, and traditional debt investments are offering lower returns. Because of this, many financial experts now suggest using 110 or even 120 minus age for better growth potential. For instance, if you are 30, using 110 minus 30 gives you 80 percent allocation to equity, which can help you build more wealth over the long term.

Benefits of this rule include:

- Easy to understand and apply without complex calculations

- Helps maintain a balanced investment strategy

- Adjusts risk automatically as you age

- Encourages long-term investing discipline

- Reduces emotional decision-making during market fluctuations

However, this rule should not be followed blindly. If your income is unstable or you are uncomfortable with market risk, you should reduce your equity exposure. Always adjust the rule based on your personal financial situation.

Use Tool: 20/4/10 Rule calculator

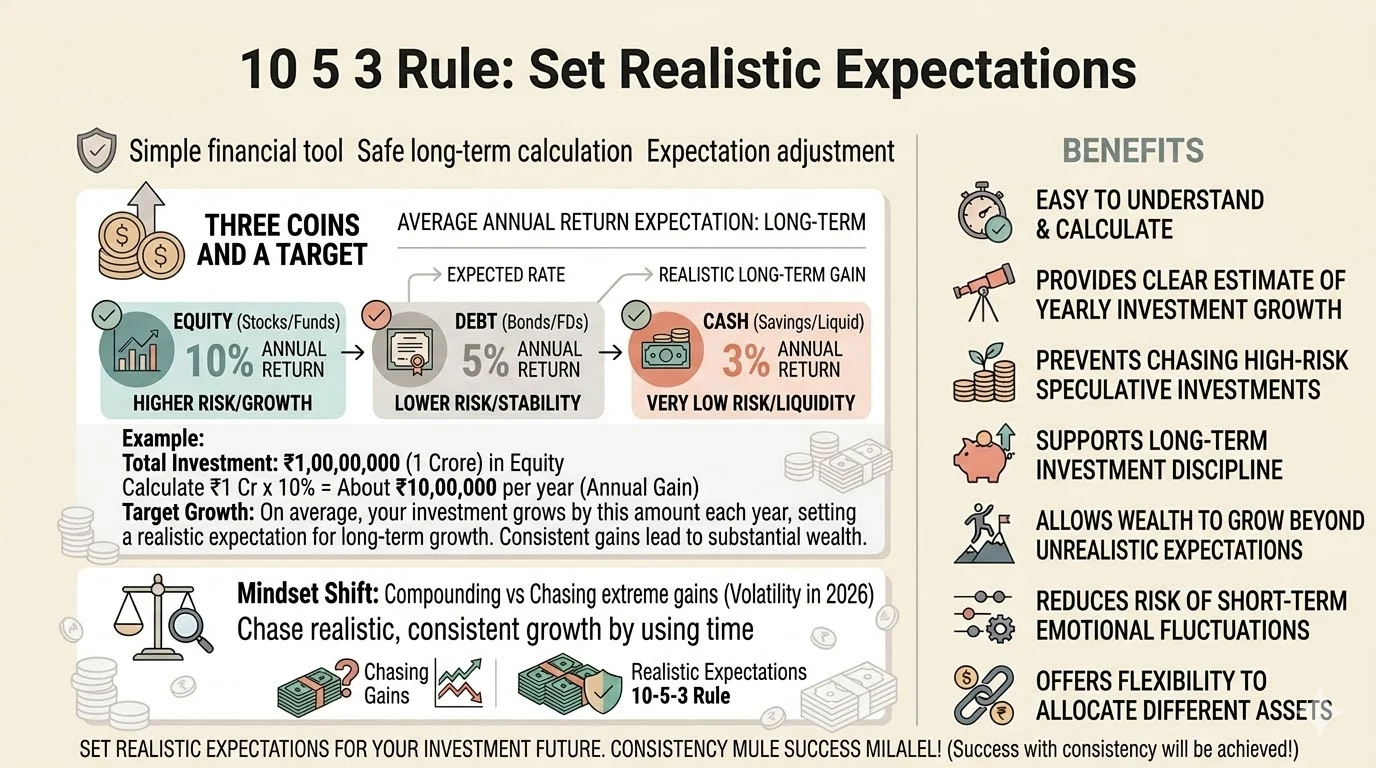

10 5 3 Rule: Set Realistic Expectations

Many people expect very high returns from their investments, especially after seeing short-term market gains or social media success stories. This often leads to disappointment when actual returns are lower or inconsistent. The 10 5 3 rule is a simple tool that helps investors set realistic expectations and avoid emotional decision-making.

The rule suggests that over the long term, different asset classes tend to deliver average returns as follows:

| Asset Type | Expected Return |

|---|---|

| Equity | 10 percent |

| Debt | 5 percent |

| Cash | 3 percent |

This means if you invest in stocks or equity mutual funds, you can expect around 10 percent annual returns over time. Debt instruments like bonds or fixed deposits may give around 5 percent, while cash or savings accounts typically offer about 3 percent.

For example, if you invest 1,00,000 in equity, you can expect it to grow to around 1,10,000 in a year on average. However, this is not guaranteed every year. Some years may give higher returns, while others may give lower or even negative returns. The rule works best when applied over a long period.

Benefits of the 10 5 3 rule:

- Sets realistic expectations and reduces disappointment

- Helps in better financial planning and goal setting

- Prevents chasing high-risk or speculative investments

- Encourages long-term investing discipline

- Makes asset allocation decisions easier

- Reduces emotional reactions during market ups and downs

In 2026, markets are more volatile and unpredictable. Having a simple framework like the 10 5 3 rule helps you stay grounded and focused on long-term wealth creation instead of short-term noise.

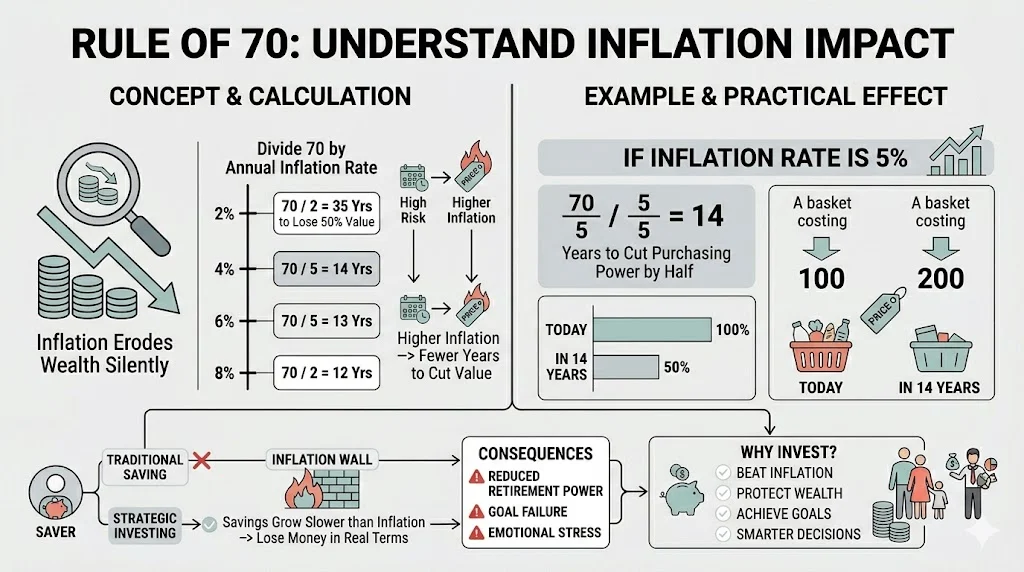

Rule Of 70: Understand Inflation Impact

Inflation silently reduces your wealth over time, and most people underestimate its long-term impact. The Rule of 70 is a simple and powerful tool that helps you understand how quickly inflation can erode the value of your money. It gives you a rough estimate of how many years it will take for your purchasing power to reduce by half.

The formula is straightforward: divide 70 by the annual inflation rate. The result tells you the number of years it will take for your money’s value to drop by 50 percent.

For example, if the inflation rate is 5 percent, you divide 70 by 5, which equals 14. This means that in 14 years, the value of your money will be cut in half. In practical terms, something that costs 100 today will cost around 200 in 14 years, assuming inflation remains constant.

This rule is especially useful for long-term financial planning. It helps you understand why simply saving money in a bank account is not enough. If your savings grow at a slower rate than inflation, you are actually losing money in real terms.

Benefits of using the Rule of 70:

- It simplifies complex financial concepts into an easy calculation

- It helps you visualize the long-term impact of inflation

- It encourages you to invest rather than just save

- It supports better retirement and goal planning

- It helps compare inflation with investment returns

By using this rule, you can make smarter decisions about where to put your money. It reminds you that to protect and grow your wealth, your investments must at least beat inflation.

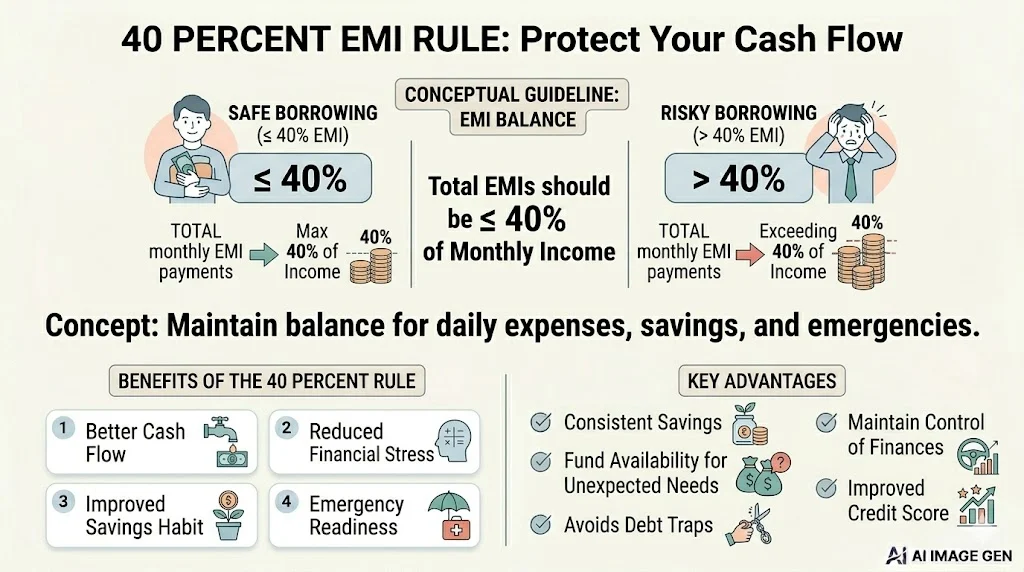

40 Percent EMI Rule: Protect Your Cash Flow

The 40 percent EMI rule is a simple but powerful guideline that helps you manage your monthly loan burden without putting your financial stability at risk. EMI stands for Equated Monthly Installment, which includes payments for home loans, car loans, personal loans, and credit card dues. According to this rule, your total EMIs should not exceed 40 percent of your monthly income. This ensures that you have enough money left for daily expenses, savings, and emergencies.

For example, if your monthly income is 50,000, your total EMI payments should ideally stay within 20,000. This means if you are already paying 15,000 as a home loan EMI, you should be cautious before taking another loan that adds more than 5,000 to your monthly burden. Staying within this limit helps you avoid financial pressure and reduces the risk of default.

Benefits of the 40 percent EMI rule:

- Better cash flow management: You always have enough money for daily expenses and lifestyle needs.

- Reduced financial stress: Lower EMI burden means less anxiety about monthly payments.

- Improved savings habit: You can consistently save and invest for future goals.

- Emergency readiness: You have funds available to handle unexpected situations without taking new loans.

- Lower risk of debt trap: You avoid over-borrowing and maintain control over your finances.

- Better credit score: Timely EMI payments improve your credit profile.

- Financial flexibility: You can take advantage of new opportunities without being overburdened by debt.

Following this rule creates a balance between borrowing and living comfortably. It ensures that loans support your life instead of controlling it.

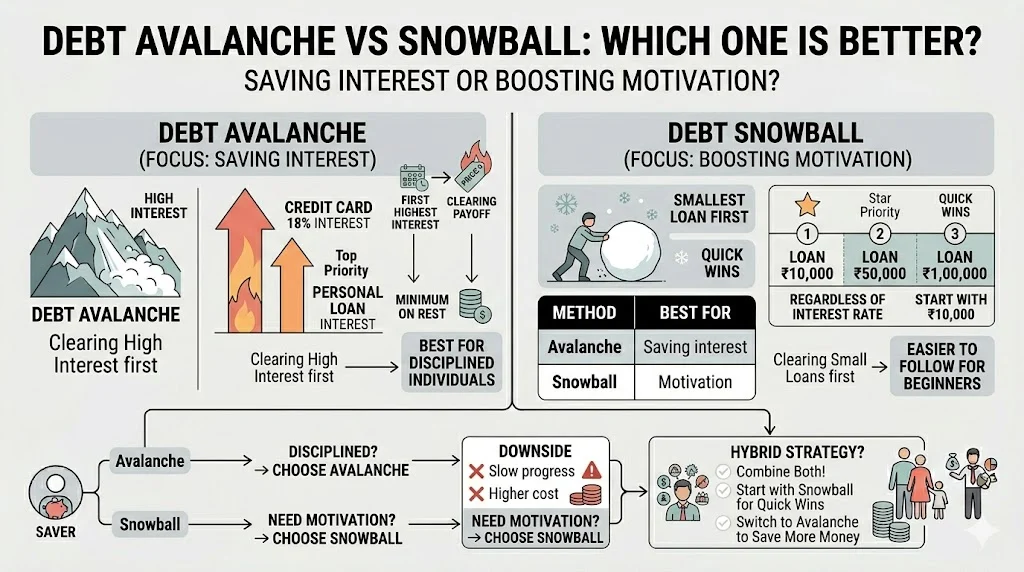

Debt Avalanche Vs Snowball: Which One Is Better?

There are two main ways to repay loans, and understanding them properly can help you choose the best strategy based on your financial situation and mindset. These methods are known as the debt avalanche method and the debt snowball method.

The debt avalanche method focuses on saving money. In this approach, you first pay off the loan with the highest interest rate while making minimum payments on other loans. Once the highest interest loan is cleared, you move to the next one. This method reduces the total interest you pay over time, making it financially efficient. For example, if you have a credit card loan at 18 percent and a personal loan at 12 percent, you should clear the credit card first.

The debt snowball method focuses on motivation. Here, you pay off the smallest loan first, regardless of interest rate. Once that loan is cleared, you move to the next smallest. This method gives quick wins, which helps you stay motivated. For example, if you have three loans of 10,000, 50,000, and 1,00,000, you start with the 10,000 loan.

Benefits of debt avalanche method:

- Saves more money on interest

- Faster long-term debt reduction

- Best for disciplined individuals

Benefits of debt snowball method:

- Builds confidence with quick results

- Keeps you motivated

- Easier to follow for beginners

| Method | Best For | Downside |

|---|---|---|

| Avalanche | Saving interest | Slow progress |

| Snowball | Motivation | Higher cost |

If you are disciplined, choose avalanche. If you need motivation, choose snowball. You can also combine both methods by starting with snowball for quick wins and then switching to avalanche to save more money.

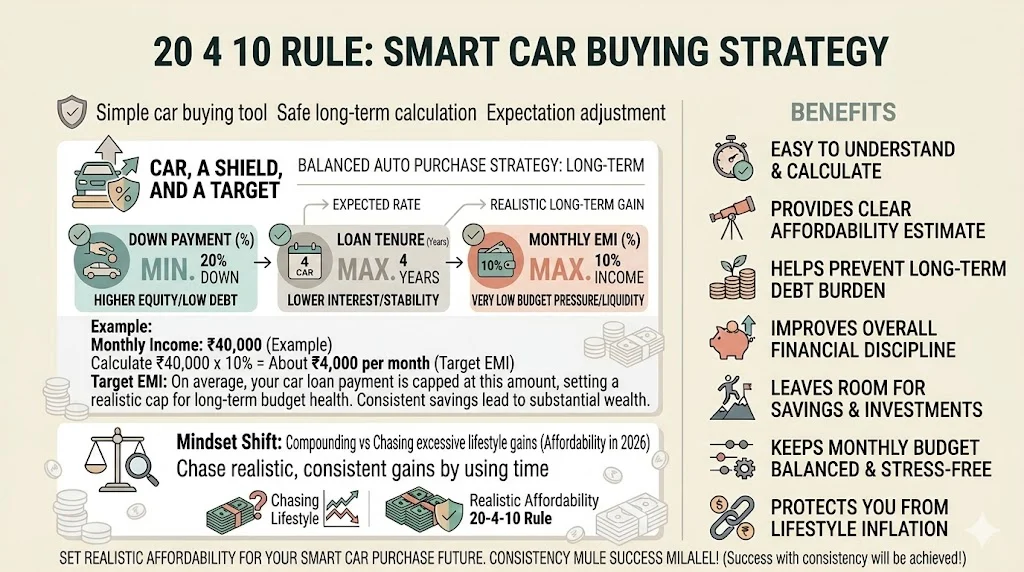

20 4 10 Rule: Smart Car Buying Strategy

Buying a car can become a financial mistake if not planned properly, especially in a time when vehicle prices and loan tenures are increasing. The 20-4-10 rule is a simple and practical guideline that helps you make a smart and affordable car purchase decision without putting pressure on your finances.

This rule has three parts. First, you should make at least a 20 percent down payment. This reduces your loan amount and interest burden. Second, your car loan tenure should not exceed 4 years. Shorter loan periods help you save on interest and avoid long-term financial commitments. Third, your monthly EMI should not be more than 10 percent of your monthly income. This ensures that your car expenses do not disturb your overall budget.

For example, if your monthly income is 40,000, your car EMI should be less than 4,000. If the EMI is higher, it means the car is too expensive for your current income level, and you should consider a cheaper option or increase your down payment.

Benefits of the 20-4-10 rule:

- Keeps your monthly budget balanced and stress-free

- Reduces total interest paid on the car loan

- Prevents long-term debt burden

- Helps you choose a car within your financial capacity

- Improves overall financial discipline

- Leaves room for savings and investments

- Protects you from lifestyle inflation

In 2026, many people are tempted to take longer loans to afford expensive cars. This often leads to financial pressure and reduced savings. By following the 20-4-10 rule, you can enjoy owning a car without compromising your financial stability.

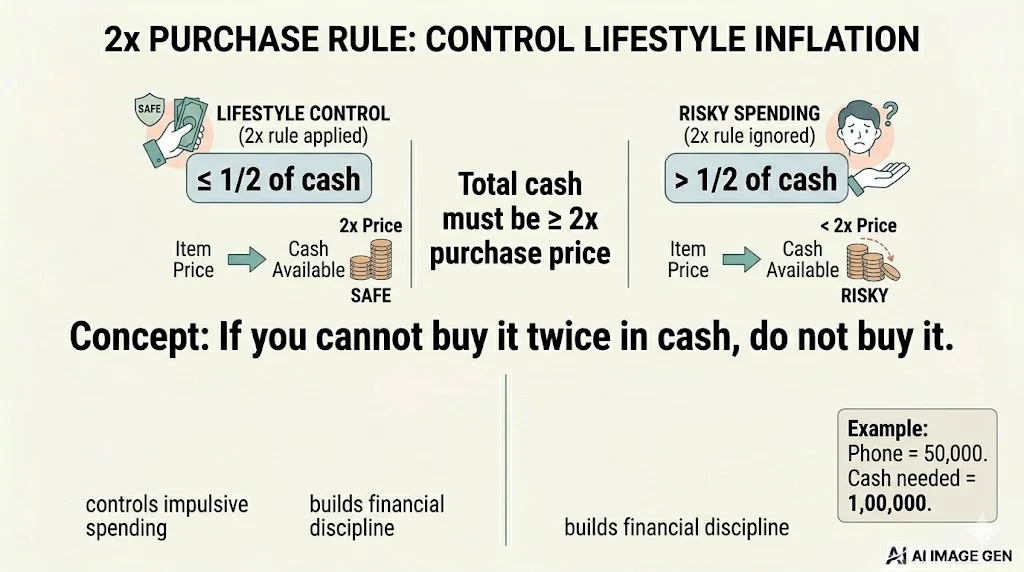

2x Purchase Rule: Control Lifestyle Inflation

Lifestyle inflation is a big problem today. This rule is simple. If you cannot buy something twice in cash, do not buy it.

Example: If a phone costs 50,000

You should have 1,00,000 available

This rule controls impulsive spending. It helps you build discipline. Many people also invest the same amount they spend. This creates balance between enjoyment and wealth.

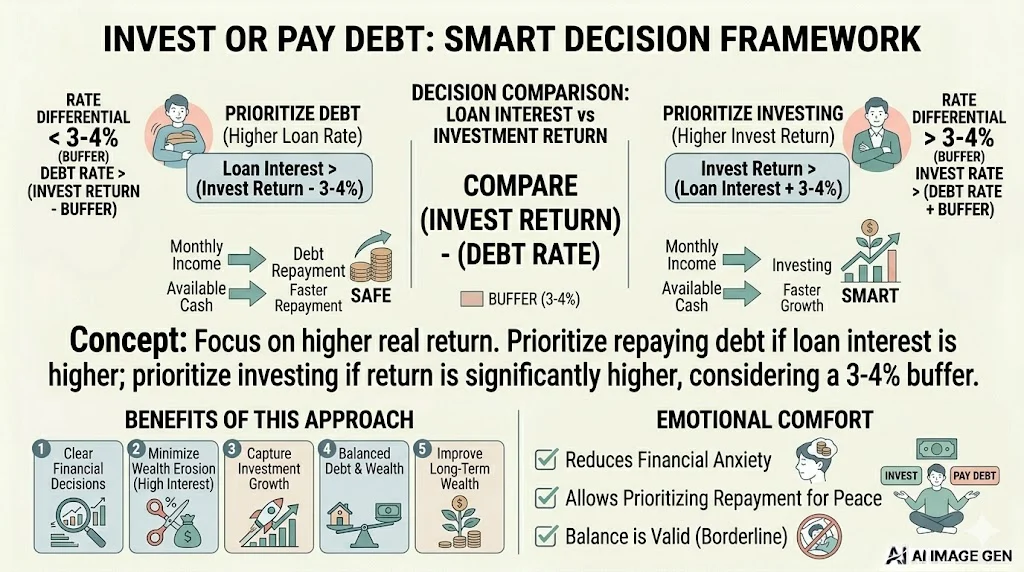

Invest Or Pay Debt: Smart Decision Framework

This is a common confusion for many people managing their finances. Deciding whether to invest or repay debt first depends on a few practical factors, not just theory.

The basic idea is simple. Compare your loan interest rate with the expected return from your investments. If your loan interest is higher than what you can realistically earn from investing, it is better to focus on repaying the debt. This is because the cost of the loan is eating into your wealth faster than your investments can grow.

On the other hand, if your expected investment return is higher than your loan interest, investing can be a smarter choice. However, you should always keep a safety buffer of 3 to 4 percent. This buffer accounts for market fluctuations, taxes, and unexpected changes in returns.

For example, if your loan interest rate is 9 percent and your expected return from investments is 12 percent, the difference is 3 percent. This is a borderline situation. In such cases, you can follow a balanced approach. You can invest a portion of your money while also making extra payments towards your loan.

Benefits of using this approach:

- Helps you make clear and logical financial decisions

- Prevents you from losing money due to high interest loans

- Allows you to take advantage of investment opportunities

- Reduces financial stress by balancing debt and growth

- Improves long term wealth creation strategy

Also, do not ignore your emotional comfort. If having debt makes you anxious or stressed, it is perfectly fine to prioritize clearing it first. Financial peace of mind is just as important as financial returns.

Emergency Fund Rule: The Missing Foundation

An emergency fund is a financial safety net that helps you handle unexpected expenses without disturbing your investments or taking new loans. It should cover 3 to 6 months of your essential expenses, and 9 to 12 months if your income is unstable. This fund is usually kept in a savings account or liquid fund for easy access. For example, if your monthly expenses are 30,000, you should keep at least 90,000 to 1,80,000 as an emergency fund. This ensures you can manage situations like job loss, medical emergencies, or urgent repairs without financial stress.

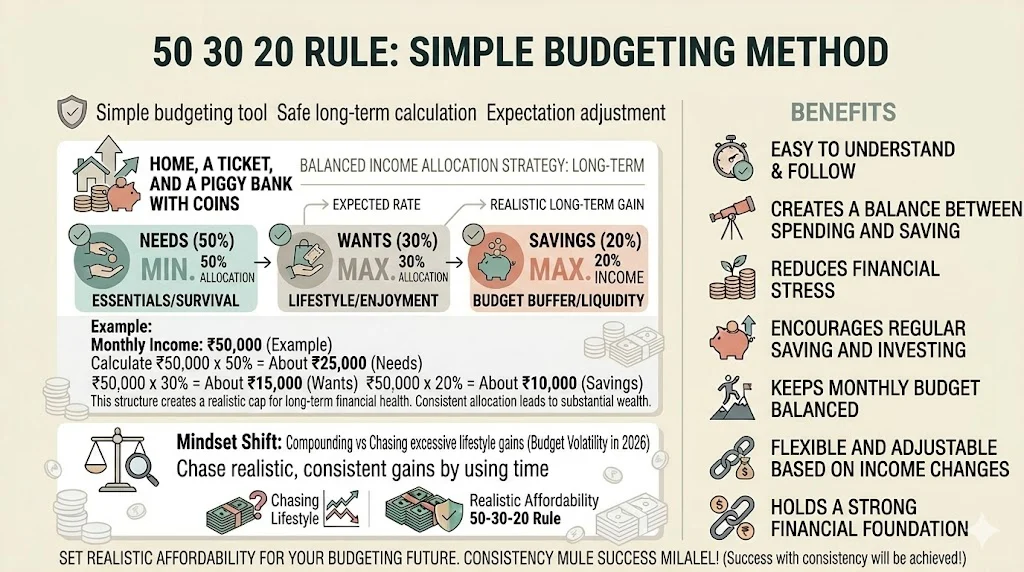

50 30 20 Rule: Simple Budgeting Method

The 50 30 20 rule is a simple and practical budgeting tool that helps you manage your income in a balanced way. It divides your monthly income into three clear categories so you can control spending, avoid financial stress, and build savings consistently. This method is especially useful for beginners who find budgeting complicated.

According to this rule, 50 percent of your income should go towards needs. These are essential expenses that you cannot avoid, such as rent, groceries, electricity bills, transportation, and basic insurance. The next 30 percent is for wants. These include lifestyle expenses like eating out, shopping, entertainment, subscriptions, and travel. The remaining 20 percent is for savings and investments. This portion helps you build an emergency fund, invest for future goals, and repay extra debt if needed.

For example, if your monthly income is 50,000, you can divide it as follows. Needs will be 25,000, wants will be 15,000, and savings will be 10,000. This clear structure helps you understand where your money is going and prevents overspending in any one area.

Benefits of the 50 30 20 rule:

- Easy to understand and follow, even for beginners

- Creates a balance between spending and saving

- Helps control unnecessary expenses

- Encourages regular saving and investing

- Reduces financial stress by setting clear limits

- Flexible and can be adjusted based on income changes

This rule gives a strong foundation for financial discipline. Over time, it helps you build better money habits and achieve long-term financial stability.

Common Mistakes People Make

Many people misuse these rules.

- They expect exact results from Rule of 72.

- They take too much risk in equity.

- They ignore inflation.

- They take high EMIs.

- They delay investing.

These mistakes reduce wealth growth.

How To Combine All These Rules In Real Life

Here is a simple plan:

- Keep EMI below 40 percent

- Build emergency fund first

- Use 110 minus age for allocation

- Invest consistently

- Follow 10 5 3 expectations

- Avoid overspending using 2x rule

- Clear high interest debt first

This combination works better than any single rule.

Real Life Example

Let us take a simple case. It is as follows:

Income is 60,000

EMI is 20,000

Savings capacity is 10,000

Step 1: Check EMI rule

20,000 is within limit

Step 2: Build emergency fund

Step 3: Invest 10,000 using proper allocation

Step 4: Avoid unnecessary expenses

Step 5: Prepay high interest loans

This simple system creates stability.

My Final Thoughts

Money rules are not shortcuts. They are guides. They help you avoid confusion. They help you take action. In 2026, financial life is complex. But your approach does not need to be complex. Simple rules can create strong results if used properly.

The real secret is consistency. Not perfection. If you follow these rules with discipline, you will see results over time. Start small. Stay consistent. Adjust when needed. That is how real wealth is built.

Related Posts :

Share This Post