Dhanlaxmi Bank Limited Share Price Target 2026, 2027, 2028, 2029, 2030, 2040, 2050

Dhanlaxmi Bank Share Price Target

Dhanlaxmi Bank is a small private sector bank based in Thrissur, Kerala. The bank offers retail banking, corporate banking, MSME loans, gold loans, and digital banking services. It also provides savings accounts, fixed deposits, and lending products for individuals and businesses. Over the last few years, the bank has shown a gradual turnaround in its financial performance.

The total income of the bank increased from around ₹1,050 crore in FY22 to nearly ₹1,450 crore in FY26. Profit also improved strongly from just ₹4.5 crore to around ₹80–90 crore in the same period. The bank has also improved its asset quality. Gross NPA has reduced to around 2.36%. Capital adequacy has increased to 17.19%, which shows better financial stability. Promoter holding remains low at around 10–13%, which is something investors should watch carefully.

Recently, the bank reported a 20% growth in profit and 21% growth in income in Q3 FY26. Business growth is also strong at around 20% YoY. Despite this, the share price is under pressure and trading near ₹21 due to weak sentiment and past performance concerns.

In this blog post we are going to see the share price target of the Dhanlaxmi Bank from year 2026-2050 from numeric & fundamental data and try to guess how much return can you expect from this share in upcoming years.

Table of Contents

Dhanlaxmi Bank Share Price Target 2026

| Month | Min Target | Max Target |

|---|---|---|

| Jan 2026 | ₹36 | ₹42 |

| Dec 2026 | ₹45 | ₹52 |

The year 2026 looks like a recovery phase for Dhanlaxmi Bank. The company has shown strong improvement in profitability. Net profit is growing and asset quality is improving. Gross NPA has reduced and capital adequacy is strong. This gives confidence that the bank is moving in the right direction.

The business growth of more than 20% is a positive signal. Deposits and advances are increasing. This shows that customers are trusting the bank again. The rise in net interest income to ₹154 crore also supports earnings growth.

However, the stock is still under pressure due to market sentiment. It has fallen from ₹33 levels to around ₹21. This shows that investors are still cautious. The bank is small in size and faces competition from large private banks.

If the bank continues to improve its asset quality and profit growth, then 2026 can be a strong recovery year. The share price may gradually move upwards as confidence returns.

Dhanlaxmi Bank Share Price Target 2027

| Month | Min Target | Max Target |

|---|---|---|

| Jan 2027 | ₹53 | ₹60 |

| Dec 2027 | ₹65 | ₹76 |

In 2027, the bank may enter a growth phase after recovery. The improvement in financials seen in 2025 and 2026 can start reflecting strongly in valuation.

The bank has already strengthened its capital base. With a capital adequacy ratio above 17%, it has room to expand its loan book. This can lead to higher interest income.

If the bank maintains control on NPAs and continues profit growth, then return ratios like ROE can improve further. Currently ROE is around 13–15%. If it crosses 15% consistently, investor confidence can increase.

Another important factor is valuation. The stock is trading at a low price to book ratio. This may attract value investors. If sentiment improves, the stock can see re-rating.

Dhanlaxmi Bank Share Price Target 2028

| Month | Min Target | Max Target |

|---|---|---|

| Jan 2028 | ₹79 | ₹90 |

| Dec 2028 | ₹100 | ₹112 |

By 2028, the bank may become more stable in terms of operations. Continuous profit growth and better margins can support long term growth.

Net profit margin has improved from below 1% to around 5–6%. This is a big improvement. If the bank maintains this margin, then earnings will grow steadily.

Technology and digital banking will also play a key role. The banking sector is becoming more digital. Smaller banks need to invest in technology to compete. If Dhanlaxmi Bank focuses on this, it can improve efficiency and customer experience. However, competition remains a major challenge. Large private banks have strong brand and reach. Dhanlaxmi Bank needs to expand its network to compete effectively.

Dhanlaxmi Bank Share Price Target 2029

| Month | Min Target | Max Target |

|---|---|---|

| Jan 2029 | ₹116 | ₹130 |

| Dec 2029 | ₹145 | ₹166 |

The year 2029 can be a strong growth year if the bank executes its strategy well. The consistent growth in revenue and profit can lead to better valuation.

The bank’s business growth of 20% is already a positive sign. If this growth continues, then total income can cross ₹2000 crore in the coming years.

Another important factor is investor sentiment. Currently, sentiment is weak due to past issues and recent price fall. But if the bank delivers consistent results, sentiment can change. Insider buying seen in March 2026 is also a positive sign. It shows that management has confidence in the business.

Dhanlaxmi Bank Share Price Target 2030

| Month | Min Target | Max Target |

|---|---|---|

| Jan 2030 | ₹170 | ₹190 |

| Dec 2030 | ₹210 | ₹245 |

By 2030, Dhanlaxmi Bank can become a stable mid-tier bank if it continues its growth journey. The bank has already improved its financial position significantly.

The key driver will be consistent profit growth. If the bank maintains profit growth of 15–20% annually, then long term investors can benefit.

Regulatory environment will also play a role. RBI norms on capital and risk management are strict. The bank’s improved capital adequacy helps it comply with these norms.

However, risks remain. The bank is small and vulnerable to economic slowdown. Any rise in NPAs can impact profitability.

Dhanlaxmi Bank Share Price Target 2040

| Month | Min Target | Max Target |

|---|---|---|

| Jan 2040 | ₹420 | ₹480 |

| Dec 2040 | ₹550 | ₹650 |

In the long term, the growth of Dhanlaxmi Bank will depend on its ability to scale. If the bank expands its branch network and digital presence, it can grow its customer base. India’s banking sector is expected to grow strongly due to economic growth. Credit demand will increase. If the bank captures even a small share of this growth, it can benefit.

The bank must focus on technology, risk management, and customer service. These factors will decide its long term success. If the bank continues to improve its fundamentals, then it can create value for long term investors.

Dhanlaxmi Bank Share Price Target 2050

| Year | Min Target | Max Target |

|---|---|---|

| 2050 | ₹850 | ₹1200 |

By 2050, the bank’s performance will depend on how it adapts to changes in the banking sector. Digital banking, fintech competition, and regulatory changes will shape the future.

If the bank successfully transforms itself into a strong digital bank, it can sustain growth. Otherwise, it may struggle against larger players. Long term investors should focus on fundamentals rather than price. The bank’s ability to grow profit, maintain asset quality, and expand business will be key.

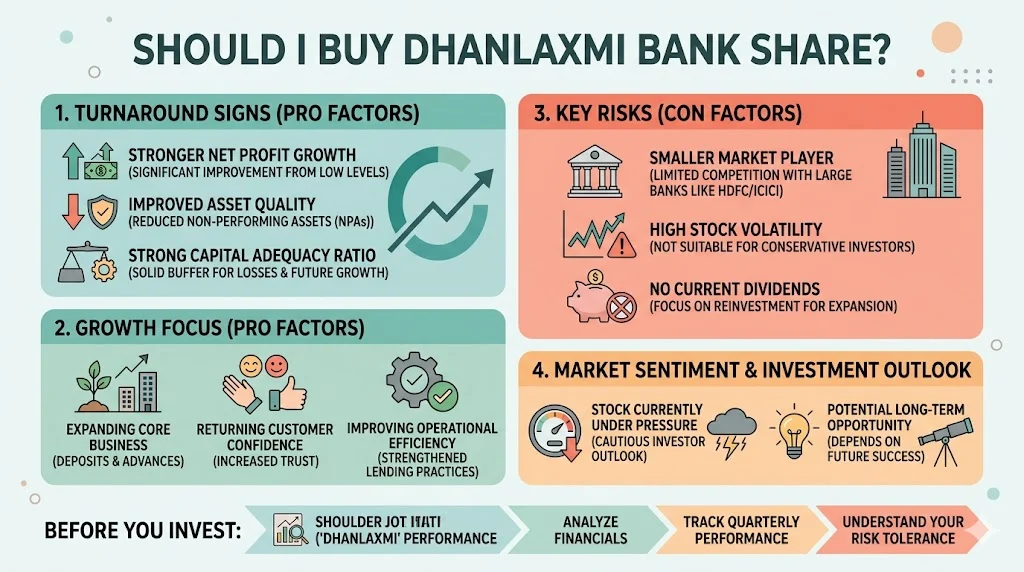

Should I Buy Dhanlaxmi Bank Share?

Dhanlaxmi Bank is often considered a turnaround story in the Indian banking sector. Over the past few years, the bank has shown a noticeable improvement in its financial performance. Its net profit has grown significantly from very low levels, and asset quality has improved with a reduction in non-performing assets (NPAs). The capital adequacy ratio is also strong, which indicates that the bank has a solid buffer to absorb potential losses and support future growth.

The bank is actively focusing on expanding its core business. Growth in deposits and advances suggests that customer confidence is gradually returning. This is an important indicator because banking is largely driven by trust. Increasing business volumes also help improve interest income and overall profitability. Additionally, the bank is working on improving operational efficiency and strengthening its lending practices, which can further support long-term growth.

However, investors should not ignore the risks involved. Dhanlaxmi Bank is still a relatively small player compared to large private sector banks like HDFC Bank or ICICI Bank. This limits its ability to compete aggressively in terms of technology, branch expansion, and product offerings. The stock has also shown high volatility in recent times, which may not suit conservative investors.

Another important point is that the bank is not currently focused on paying dividends. Instead, it is reinvesting its earnings to strengthen its balance sheet and support future expansion. While this may not appeal to income-focused investors, it can be beneficial for long-term capital appreciation.

Market sentiment also plays a crucial role. The stock is currently under pressure due to past concerns and overall cautious investor outlook. This could present a potential buying opportunity for long-term investors, but it also reflects underlying risks.

Before investing, it is important to analyze financials, track quarterly performance, and understand your own risk tolerance.

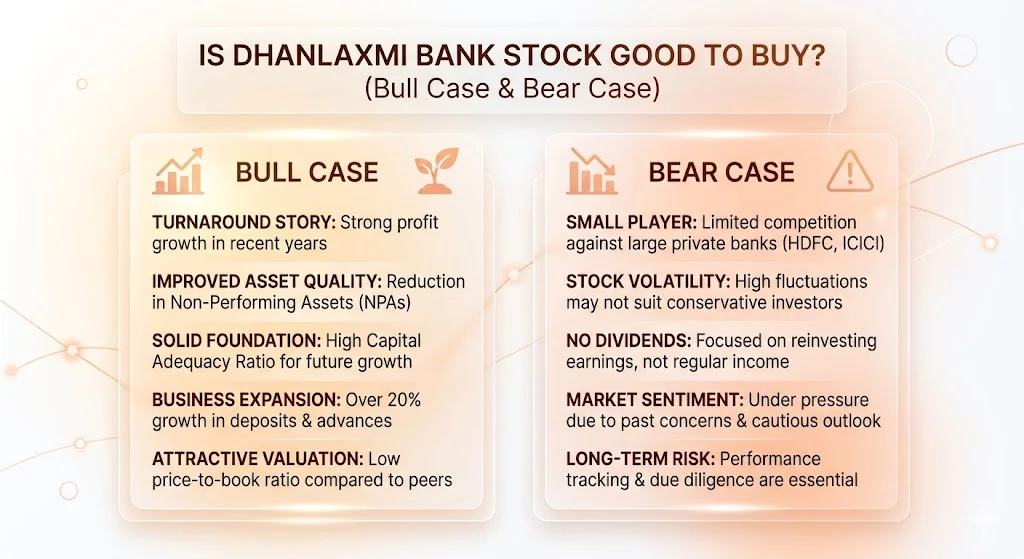

Is Dhanlaxmi Bank Stock Good to Buy (Bull Case & Bear Case)

Bull Case:

- Strong profit growth in recent years

- Improvement in asset quality (low NPA)

- High capital adequacy ratio

- Business growth above 20%

- Low valuation may attract investors

The bull case for Dhanlaxmi Bank is primarily driven by its turnaround story. Over the past few years, the bank has shown a sharp improvement in profitability, moving from negligible profits to a stable earnings trajectory. This indicates better operational efficiency and improved management focus. The reduction in NPAs is another strong positive, as asset quality is one of the most critical factors for any banking institution. Lower NPAs directly improve profitability and reduce risk.

Additionally, the bank’s capital adequacy ratio above regulatory requirements provides a strong cushion for future expansion. This allows the bank to grow its loan book without immediate need for capital infusion. The consistent business growth of over 20% in deposits and advances shows increasing customer trust and expanding market presence.

Another important factor is valuation. The stock is currently trading at a relatively low price-to-book ratio compared to peers. If the bank continues to deliver consistent financial performance, there is a possibility of valuation re-rating, which can lead to significant upside for long-term investors.

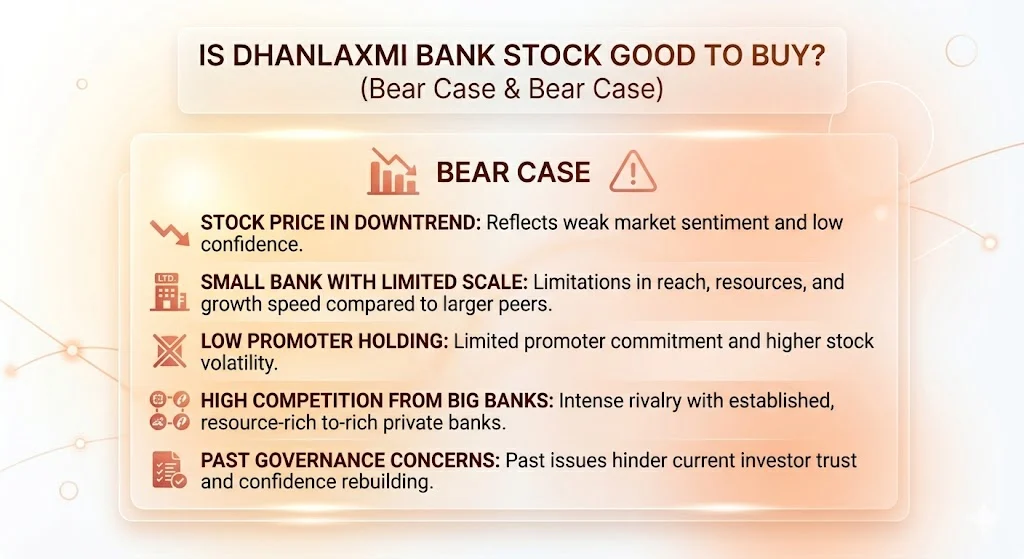

Bear Case:

- Stock price in downtrend

- Small bank with limited scale

- Low promoter holding

- High competition from big banks

- Past governance concerns

Despite the positives, there are several risks that investors should consider. The stock has been in a downtrend recently, which reflects weak market sentiment and lack of strong investor confidence. Being a small-sized bank, Dhanlaxmi Bank faces limitations in terms of scale, reach, and resources compared to larger private sector banks.

Low promoter holding is another concern, as it may indicate limited promoter commitment and can lead to higher volatility in stock price. The banking sector is highly competitive, with large players having strong digital infrastructure, brand value, and customer base. Competing with such institutions can be challenging for a smaller bank.

Additionally, past governance issues have impacted investor trust. Although the bank has improved its performance, rebuilding long-term confidence takes time. Any negative developments in governance or asset quality can quickly impact the stock.

Promoters Holding Of Dhanlaxmi Bank

| Year | Holding |

|---|---|

| FY22 | ~12% |

| FY23 | ~12% |

| FY24 | ~13% |

| FY25 | ~12% |

| FY26 | ~10–13% |

Promoter holding in Dhanlaxmi Bank is relatively low compared to many other private sector banks. As seen in the table above, promoter stake has remained in the range of around 10–13% over the past few years, without any significant increase.

This indicates that promoters do not have strong controlling power in the company. In the banking sector, higher promoter holding is generally preferred because it reflects long-term commitment and confidence of the promoters in the business.

Low promoter holding can sometimes lead to higher volatility in the stock price, as ownership is more widely distributed among public and institutional investors. It also increases dependence on institutional investors for stability and decision-making. However, stable promoter holding without continuous decline is still a positive sign. Investors should monitor any major changes in promoter stake, as it can impact overall sentiment and governance perception.

Revenue Growth Of Dhanlaxmi Bank

| Year | Revenue | Growth |

|---|---|---|

| FY22 | ₹1050 Cr | 16% |

| FY23 | ₹1260 Cr | 20% |

| FY24 | ₹1320 Cr | 5% |

| FY25 | ₹1437 Cr | 9% |

| FY26 | ₹1450+ Cr | 1–3% |

Revenue growth is stable but not very high. As seen in the table above, the bank has shown consistent improvement in revenue from ₹1050 crore in FY22 to around ₹1450 crore in FY26. However, the growth rate has been uneven, with strong growth in FY23 followed by slower expansion in subsequent years. This indicates that while the bank is able to maintain its income levels, it is not yet achieving aggressive expansion like larger private sector banks.

The slowdown in growth during FY24 and FY26 suggests challenges in scaling operations or increasing lending at a faster pace. To compete effectively with peers, the bank needs to focus on expanding its loan book, improving fee-based income, and strengthening its digital banking services. Sustained higher revenue growth will be important for improving profitability and attracting long-term investors.

Profit Growth (CAGR%) Of Dhanlaxmi Bank

| Year | Profit | Growth |

|---|---|---|

| FY22 | ₹4.5 Cr | High |

| FY23 | ₹15.5 Cr | 240% |

| FY24 | ₹35 Cr | 125% |

| FY25 | ₹84 Cr | 140% |

| FY26 | ₹80–90 Cr | Stable |

Profit growth is very strong, as clearly reflected in the above table. The bank has moved from a very low profit base of ₹4.5 crore in FY22 to around ₹80–90 crore in FY26, which indicates a significant turnaround in its financial performance. This consistent increase in profits over the years shows that the bank has successfully improved its operational efficiency and managed its costs effectively.

The sharp rise in profit growth percentages, especially between FY23 and FY25, highlights strong recovery momentum.

It also suggests better asset quality, improved loan recovery, and controlled NPAs. Such growth is important for rebuilding investor confidence, especially after years of weak performance. If the bank continues this trend, it can further strengthen its balance sheet and improve return ratios like ROE. Sustained profit growth will also support long-term valuation improvement and attract more institutional investors.

EPS or ROE Trends Of Dhanlaxmi Bank

| Year | EPS | ROE |

|---|---|---|

| FY22 | 0.2 | 2% |

| FY23 | 0.5 | 4% |

| FY24 | 1.0 | 8% |

| FY25 | 2.1 | 13% |

| FY26 | 2.3 | 15% |

ROE is improving steadily over the years, which reflects the bank’s strengthening profitability and better utilization of shareholder funds. Starting from a very low level of around 2% in FY22, the return on equity has gradually increased to nearly 15% by FY26. This consistent rise indicates that the bank has successfully improved its earnings while maintaining a stable capital base.

Higher ROE generally attracts investors because it shows that the company is generating better returns on invested capital. The improvement is mainly driven by rising net profits, better asset quality, and controlled operating costs.

If the bank continues this trend and sustains ROE above 15%, it can significantly boost investor confidence and valuation. However, maintaining this level will depend on consistent profit growth and effective risk management in the coming years.

Debt-to-Equity Ratio Of Dhanlaxmi Bank

| Year | Status |

|---|---|

| FY22 | High |

| FY23 | High |

| FY24 | Moderate |

| FY25 | Moderate |

| FY26 | Stable |

For banks, this is normal because their business model is based on borrowing funds (deposits) and lending them at higher interest rates. Unlike manufacturing companies, banks naturally operate with higher leverage.

In the case of Dhanlaxmi Bank, the debt-to-equity ratio has gradually improved from high levels in earlier years to a more stable position in FY26. This indicates better balance sheet management and controlled risk exposure.

A stable ratio suggests that the bank is not excessively dependent on borrowed funds beyond industry norms. It also reflects improved capital adequacy and prudent lending practices. Investors should not view high debt in banks negatively without context, but they should monitor trends. If the ratio continues to stabilize or improve, it can support long-term growth and financial stability for the bank.

Net Profit Margins Of Dhanlaxmi Bank

| Year | Margin |

|---|---|

| FY22 | 0.5% |

| FY23 | 1.3% |

| FY24 | 2.8% |

| FY25 | 5.8% |

| FY26 | ~5.5% |

Margins are improving strongly, as seen in the steady rise from just 0.5% in FY22 to around 5.5% in FY26. This consistent improvement reflects better cost control, higher interest income, and improved asset quality. As the bank reduces its non-performing assets, it is able to retain more earnings, which directly supports margin expansion. Additionally, growth in advances and deposits has helped increase net interest income, further strengthening profitability.

The bank’s focus on efficient operations and disciplined lending is also contributing to this positive trend. If this momentum continues, margins can stabilize at higher levels in the coming years. However, sustaining these margins will depend on maintaining asset quality and managing operating expenses effectively.

Market Capitalization Of Dhanlaxmi Bank

| Year | Market Cap |

|---|---|

| 2021 | ₹350 Cr |

| 2022 | ₹450 Cr |

| 2023 | ₹650 Cr |

| 2024 | ₹850 Cr |

| 2025 | ₹1000 Cr |

| 2026 | ₹900 Cr |

Small market capitalization indicates that Dhanlaxmi Bank is still in its early growth phase compared to larger banking peers. As seen in the table, the market cap has gradually increased from ₹350 crore in 2021 to around ₹1000 crore in 2025, showing improving investor confidence. However, the slight decline to ₹900 crore in 2026 reflects recent market pressure and volatility in the stock price.

Small-cap stocks like this often experience sharp price movements due to lower liquidity and higher sensitivity to market sentiment. While this increases risk, it also creates opportunities for higher returns if the company continues its turnaround and growth trajectory. Investors should closely monitor financial performance and market trends before investing.

Dividend Yield Of Dhanlaxmi Bank

| Year | Dividend |

|---|---|

| FY22 | 0 |

| FY23 | 0 |

| FY24 | 0 |

| FY25 | 0 |

| FY26 | 0 |

The bank does not pay dividend.

My Final Words On Dhanlaxmi Bank

Dhanlaxmi Bank is a turnaround story in the Indian banking sector. The bank has improved its financial performance in recent years. Profit growth is strong and asset quality is better. Capital adequacy is also strong which gives stability.

However, the bank is still small compared to other private banks. It faces strong competition. The stock is also volatile and currently under pressure. For long term investors, the bank can be an interesting opportunity if it continues to improve its fundamentals. But risk is also high.

Investors should track key factors like profit growth, NPA levels, and business expansion. These will decide the future performance of the stock. Always invest carefully and do your own research before making any decision.

Related Posts :

Share This Post