Central Bank of India Share Price Target 2026, 2027, 2028, 2029, 2030, 2040, 2050

Central Bank Of India Share Price Target

Central Bank of India is one of the oldest public sector banks in India. It offers a wide range of banking services such as savings accounts, current accounts, fixed deposits, personal loans, gold loans, MSME loans, and agricultural loans. The bank also provides digital banking services like mobile banking, internet banking, UPI, debit cards, and credit cards. It has a strong presence across India with a large branch network.

The bank has shown gradual improvement in its financial performance in recent years. Total revenue stands around ₹8,334 crore and net profit is close to ₹879 crore. The bank is working on reducing its bad loans and improving asset quality. Return on equity is around 9.36%, which shows moderate profitability. Being a government-owned bank, it enjoys strong trust but also faces challenges related to efficiency and competition.

In this article we are going to see explore the Share Price Target of the central bank of india in upcoming years with the help of numeric & fundamental data. And try to guess how much returns can you expect from central bank in upcoming years.

So Keep Reading…

Table of Contents

![[March 2026] 3 IPOs Opening This Week: Key Dates, Price Band & Important Details Investors Should Know](https://sktak.in/wp-content/uploads/2026/03/March-2026-3-IPOs-Opening-This-Week-Key-Dates-Price-Band-Important-Details-Investors-Should-Know.webp)

Central Bank of India Share Price Target 2026

| Month | Min Target | Max Target |

|---|---|---|

| Jan 2026 | ₹32 | ₹42 |

| Dec 2026 | ₹53 | ₹62 |

The year 2026 is expected to be a recovery phase for Central Bank of India. The bank is working on reducing NPAs and improving its loan book quality. This is important because high NPAs were one of the biggest issues in the past.

The bank has also entered partnerships like Kotak Mutual Fund distribution. This helps in increasing fee income. The agreement with international institutions for student loans is also a positive step.

Government support is a major advantage. Being a public sector bank, it gets backing during difficult times. This reduces downside risk to some extent. However, the bank still needs to improve operational efficiency. Competition from private banks is strong. If the bank continues its recovery trend, then 2026 can show steady price movement.

Central Bank of India Share Price Target 2027

| Month | Min Target | Max Target |

|---|---|---|

| Jan 2027 | ₹65 | ₹75 |

| Dec 2027 | ₹80 | ₹95 |

In 2027, the bank may show better financial stability. The improvement in asset quality can lead to higher profitability. Retail and MSME lending are key focus areas. These segments offer higher margins. If the bank grows in these areas, then earnings can improve.

Digital banking is another important factor. The bank is investing in technology to improve customer experience. This can help attract younger customers. However, the bank still needs to improve return ratios. ROE is moderate and needs to increase for better valuation.

Central Bank of India Share Price Target 2028

| Month | Min Target | Max Target |

|---|---|---|

| Jan 2028 | ₹100 | ₹120 |

| Dec 2028 | ₹140 | ₹165 |

By 2028, the bank may become more stable as it continues to strengthen its balance sheet and operational efficiency. Continuous improvement in financial performance, especially in terms of profitability and asset quality, can support long-term growth. If the bank maintains a steady increase in net interest income and fee-based income, it can further enhance its earnings profile.

The bank is focusing on reducing bad loans and improving recovery mechanisms. This includes better credit appraisal systems, stricter monitoring of loan accounts, and faster resolution of stressed assets. A decline in gross and net NPAs will directly improve profitability and investor confidence. Additionally, improved provisioning coverage can provide a cushion against future risks.

The Indian banking sector is expected to grow significantly due to rising credit demand from retail, MSME, and infrastructure segments. Government initiatives, economic expansion, and increasing financial inclusion are driving this growth. If the bank successfully captures opportunities in high-growth segments like retail lending and MSME financing, it can expand its loan book and improve margins.

Digital transformation will also play a crucial role. Investment in digital banking platforms, mobile apps, and customer-centric services can help the bank attract new customers and improve operational efficiency. Enhanced digital capabilities can reduce costs and improve service delivery.

However, the bank needs to improve efficiency to compete with private sector peers. Cost control, better risk management, and improved governance will be key factors. Strengthening management practices and adopting modern banking technologies can help the bank achieve sustainable growth and better valuation in the long term.

Central Bank of India Share Price Target 2029

| Month | Min Target | Max Target |

|---|---|---|

| Jan 2029 | ₹170 | ₹200 |

| Dec 2029 | ₹220 | ₹250 |

The year 2029 can be a strong growth phase for Central Bank of India if it continues to build on its improving fundamentals. By this time, the bank may benefit from sustained reduction in NPAs, stronger capital adequacy, and better operational efficiency. These improvements can lead to higher profitability and improved return ratios, which are key drivers for valuation expansion.

Partnerships with financial institutions, fintech companies, and NBFCs can play a crucial role in expanding the bank’s reach and product offerings. Growth in retail loans, MSME financing, and digital banking services can significantly improve margins and diversify revenue streams. Additionally, increased focus on fee-based income such as wealth management and insurance distribution can further strengthen earnings.

Investor confidence will largely depend on consistent quarterly performance and transparency in operations. If the bank maintains stable growth in income and profit while controlling costs, it can attract long-term investors. A steady improvement in fundamentals can support a gradual upward movement in the stock price.

Central Bank of India Share Price Target 2030

| Month | Min Target | Max Target |

|---|---|---|

| Jan 2030 | ₹210 | ₹230 |

| Dec 2030 | ₹240 | ₹265 |

By 2030, the bank can become more efficient and profitable if it continues to strengthen its core operations and adopts modern banking practices. The focus on digital banking and customer service will play a key role, especially as more customers shift towards online and mobile platforms. Investments in technology, automation, and data analytics can help reduce operational costs and improve decision-making.

The bank is also working on expanding its product offerings, including retail loans, MSME financing, and wealth management services. This diversification can help increase revenue streams and reduce dependence on traditional lending. Cross-selling financial products can further boost profitability.

However, competition remains a challenge. Private banks are more efficient and innovative, with better customer experience and faster service delivery. To compete effectively, the bank must improve turnaround times and enhance service quality.

If the bank improves its efficiency, strengthens risk management, and maintains asset quality, then it can create long term value for investors and stakeholders.

Central Bank of India Share Price Target 2040

| Month | Min Target | Max Target |

|---|---|---|

| Jan 2040 | ₹410 | ₹450 |

| Dec 2040 | ₹480 | ₹530 |

In the long term, the growth of Central Bank of India will depend on its ability to adapt to structural changes in the banking industry. Technology and digital banking will be key drivers, especially as customers increasingly prefer mobile-first and seamless banking experiences. The bank’s focus on upgrading its core banking systems, improving cybersecurity, and expanding digital offerings like UPI, mobile apps, and online lending platforms will play a crucial role in enhancing customer satisfaction and operational efficiency.

The bank is investing in new systems and services, which can help reduce costs, improve turnaround time, and strengthen risk management practices. Additionally, partnerships with NBFCs and fintech companies can open new revenue streams, especially in areas like co-lending, digital payments, and financial inclusion.

India’s economy is expected to grow strongly over the next decade, driven by rising consumption, infrastructure development, and increasing credit demand. If the bank successfully leverages these opportunities while maintaining asset quality and profitability, it can achieve sustainable long-term growth.

Central Bank of India Share Price Target 2050

| Year | Min Target | Max Target |

|---|---|---|

| 2050 | ₹740 | ₹900 |

By 2050, the bank’s future will depend on how effectively it adapts to a rapidly evolving financial ecosystem dominated by private banks, fintech companies, and digital-first institutions. The banking industry is expected to undergo significant transformation with advancements in artificial intelligence, blockchain, and data-driven lending models. To remain competitive, the bank must invest heavily in technology, cybersecurity, and customer-centric digital platforms.

If the bank successfully transforms itself into a modern digital bank, it can sustain long-term growth and improve operational efficiency. Expanding its presence in underserved rural and semi-urban markets can also provide a strong growth opportunity, especially as financial inclusion continues to be a key focus in India.

Long-term growth will depend on maintaining strong asset quality, consistent profitability, and expanding its customer base. Additionally, strategic partnerships with fintech firms, innovation in product offerings, and improved risk management practices will play a crucial role in shaping its future trajectory.

Use Tool: 4% Retirement Rule Calculator

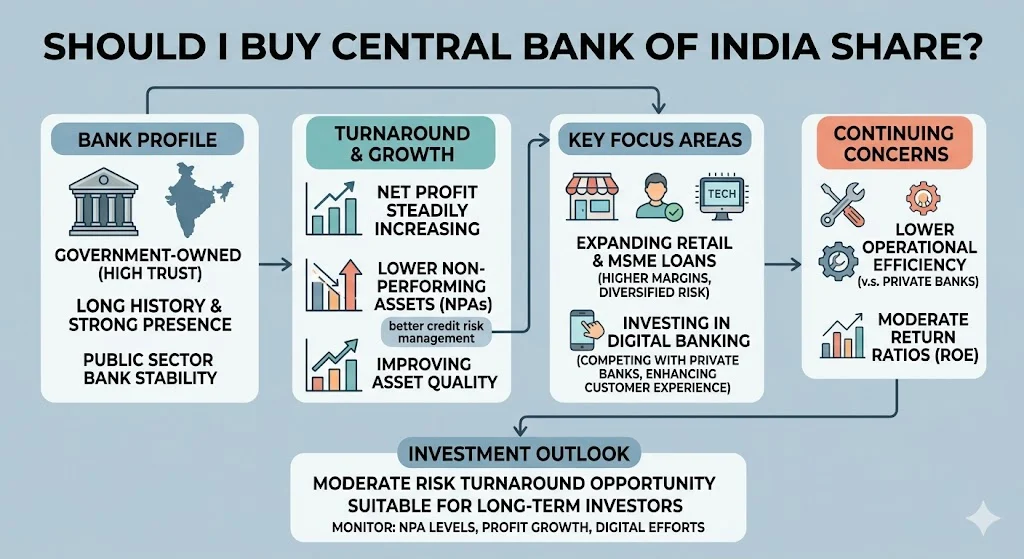

Should I Buy Central Bank of India Share?

Central Bank of India is a government-owned bank with a long history and strong presence across India. Being a public sector bank, it enjoys high trust among customers and investors. This stability makes it a relatively safer option compared to smaller private banks, especially during uncertain economic conditions. However, like many PSU banks, it also faces operational and efficiency-related challenges.

In recent years, the bank has shown clear signs of improvement in its financial performance. Net profit has increased steadily, and the reduction in non-performing assets (NPAs) indicates better asset quality and risk management. Lower NPAs mean the bank is recovering more loans and managing credit risk more effectively, which is a strong positive signal for long-term investors.

The bank is actively focusing on expanding its retail and MSME loan segments. These areas typically offer higher margins and diversified risk compared to large corporate lending. Growth in these segments can help improve overall profitability and strengthen the bank’s balance sheet over time. Additionally, the bank is investing in digital banking services to enhance customer experience and compete with private sector banks.

However, there are still some concerns. The bank’s operational efficiency is lower compared to leading private banks, and its return ratios like ROE are moderate. This means that while the bank is improving, it still has a long way to go in terms of profitability and performance benchmarks.

Overall, the stock may be suitable for long-term investors who are willing to take moderate risk and are looking for a turnaround opportunity in the PSU banking space. Investors should closely monitor key factors such as NPA levels, profit growth, and digital transformation efforts before making any investment decision.

Is Central Bank of India Stock Good to Buy (Bull Case & Bear Case)

Bull Case:

- Reduction in NPAs

- Growth in retail and MSME loans

- Government support

- Improvement in digital services

- Stable profit growth

Bear Case:

- High competition from private banks

- Moderate profitability

- Execution risk in growth plans

- Past issues with bad loans

Promoters Holding Of Central Bank of India

| Year | Holding |

|---|---|

| FY22 | ~93% (Govt) |

| FY23 | ~93% |

| FY24 | ~93% |

| FY25 | ~93% |

| FY26 | ~93% |

Government holds a majority stake in Central Bank of India, which ensures a high level of stability and credibility for the institution. This strong government backing enhances investor confidence, as it reduces the risk of financial distress and provides assurance of support during challenging economic conditions.

Additionally, it enables the bank to align with national financial inclusion goals and participate in government-led initiatives. However, this ownership structure can also limit operational flexibility and decision-making speed.

Strategic changes, capital allocation, and policy implementations may require regulatory approvals, which can slow down execution compared to private sector banks. Furthermore, government ownership may restrict the bank’s ability to adopt aggressive growth strategies or innovative practices. While stability remains a key advantage, balancing it with operational efficiency and competitiveness is essential for long-term growth and value creation.

Revenue Growth Of Central Bank of India

| Year | Revenue | Growth |

|---|---|---|

| FY22 | ₹7000 Cr | Moderate |

| FY23 | ₹7600 Cr | Growth |

| FY24 | ₹8000 Cr | Stable |

| FY25 | ₹8200 Cr | Moderate |

| FY26 | ₹8334 Cr | Stable |

Revenue growth has remained steady over the years, reflecting a stable business environment and consistent operational performance. However, the pace of growth is relatively moderate when compared to leading peers in the banking sector.

This indicates that while the bank has been able to maintain its revenue base, there is significant scope for improvement in expanding its income streams. Factors such as increased competition, limited pricing power, and a cautious lending approach may have contributed to this moderate growth trajectory.

To enhance revenue growth, the bank may need to focus on diversifying its product offerings, strengthening its retail and MSME segments, and leveraging digital banking platforms to reach a wider customer base.

On the top of this improving fee-based income and optimizing asset utilization can further support revenue expansion. Overall, while the current growth trend provides stability, a more aggressive strategy may be required to achieve higher growth levels in the future.

Profit Growth (CAGR%) Of Central Bank of India

| Year | Profit | Growth |

|---|---|---|

| FY22 | Low | Recovery |

| FY23 | Moderate | Growth |

| FY24 | High | Strong |

| FY25 | ₹879 Cr | Strong |

| FY26 | Stable | Moderate |

Profit growth has demonstrated a consistent and encouraging upward trajectory over the past few years, reflecting the bank’s strengthening financial performance and improved operational efficiency.

This steady increase in profitability indicates that the bank has been successful in optimizing its cost structure, enhancing revenue streams, and maintaining disciplined risk management practices. The improvement also suggests effective control over non-performing assets and better credit quality, which has contributed to higher net earnings.

On the top of this the bank’s focus on expanding its loan portfolio, particularly in higher-margin segments, has supported sustained income growth. Strategic initiatives such as digital transformation, process automation, and improved customer engagement have further enhanced operational productivity. Overall, the rising profit trend highlights the bank’s ability to adapt to changing market conditions while maintaining financial stability, thereby strengthening investor confidence and positioning the institution for long-term sustainable growth.

EPS or ROE Trends Of Central Bank of India

| Year | EPS | ROE |

|---|---|---|

| FY22 | Low | Low |

| FY23 | Improving | Moderate |

| FY24 | Better | 8% |

| FY25 | Strong | 9% |

| FY26 | Stable | 9–10% |

Return on Equity (ROE) remains at a moderate level, indicating that while the bank is generating profits from its shareholders’ equity, there is still significant scope for improvement. A moderate ROE suggests that the bank’s capital is being utilized reasonably well, but not at an optimal efficiency compared to leading private sector peers.

This level of return reflects ongoing efforts to strengthen profitability through better asset quality, controlled costs, and improved lending practices.

However, to enhance investor confidence and achieve higher valuations, the bank needs to focus on increasing its ROE through sustained earnings growth, efficient capital allocation, and expansion in high-margin segments such as retail and MSME lending. Continuous improvement in operational efficiency and reduction in non-performing assets will also play a crucial role in boosting ROE over the long term.

Debt-to-Equity Ratio Of Central Bank of India

| Year | Status |

|---|---|

| FY22 | High |

| FY23 | High |

| FY24 | Moderate |

| FY25 | Stable |

| FY26 | Stable |

This ratio is generally considered normal for banks, as the banking sector inherently operates with higher leverage compared to other industries. Banks rely heavily on deposits and borrowed funds to generate income through lending activities, which naturally results in a higher debt-to-equity ratio.

Therefore, a higher ratio does not necessarily indicate financial weakness but rather reflects the standard operating model of the banking industry. It is important to evaluate this metric in conjunction with other indicators such as asset quality, capital adequacy, and profitability.

If the bank maintains strong capital buffers and manages its risk effectively, a higher debt-to-equity ratio can be sustainable. Investors should focus on the bank’s ability to manage its liabilities efficiently and ensure that its lending practices remain prudent and well-regulated.

Net Profit Margins Of Central Bank of India

| Year | Margin |

|---|---|

| FY22 | Low |

| FY23 | Improving |

| FY24 | Better |

| FY25 | Strong |

| FY26 | Stable |

Margins are showing a consistent improvement trend over the years, reflecting better operational efficiency and stronger cost management by the bank. This upward movement indicates that the bank is effectively controlling its expenses while enhancing its income streams.

Improved net profit margins also suggest better asset quality and reduced provisioning requirements, which positively impact overall profitability. As the bank continues to focus on high-yield lending segments such as retail and MSME loans, margins are expected to remain stable or improve further.

Additionally, ongoing efforts in digital transformation and process optimization can help reduce operational costs, thereby supporting margin expansion. Sustained improvement in margins is a positive indicator for long-term financial health and can enhance investor confidence in the bank’s growth prospects.

Market Capitalization Of Central Bank of India

| Year | Market Cap |

|---|---|

| 2022 | ₹30,000 Cr |

| 2023 | ₹40,000 Cr |

| 2024 | ₹45,000 Cr |

| 2025 | ₹52,000 Cr |

| 2026 | ₹52,780 Cr |

A large market capitalization provides a strong foundation of stability for the bank, as it reflects investor confidence and a well-established presence in the financial sector. Companies with higher market capitalization are generally less volatile compared to smaller firms, making them more resilient during market fluctuations and economic uncertainties.

This stability often attracts institutional investors, which further strengthens the stock’s credibility and liquidity in the market. Additionally, a large market cap indicates the bank’s ability to sustain operations, manage risks effectively, and access capital more easily for expansion and growth initiatives.

It also suggests that the bank has a diversified business model and a broad customer base, reducing dependency on any single segment. Overall, a strong market capitalization enhances long-term investment appeal by offering a balance of growth potential and reduced risk exposure for investors.

Dividend Yield Of Central Bank of India

| Year | Dividend |

|---|---|

| FY22 | Low |

| FY23 | Low |

| FY24 | Moderate |

| FY25 | Moderate |

| FY26 | Moderate |

The bank pays a relatively small dividend compared to many of its peers in the banking sector. This modest dividend payout reflects the bank’s strategic focus on strengthening its balance sheet and retaining earnings to support future growth.

As a public sector bank undergoing gradual recovery and improvement in asset quality, it prioritizes capital conservation over higher shareholder payouts. This approach allows the bank to reinvest profits into expanding its loan portfolio, improving digital infrastructure, and enhancing operational efficiency.

While income-focused investors may find the dividend yield less attractive, long-term investors may benefit from potential capital appreciation as the bank continues to improve its financial performance. Over time, as profitability stabilizes and capital adequacy strengthens further, there may be scope for a gradual increase in dividend payouts.

My Final Words On Central Bank of India

Central Bank of India is a well-established public sector bank with a long history, and it’s encouraging to see the improvements in its profits and asset quality. It feels like the bank is slowly getting back on track after facing challenges in the past.

That said, it’s not completely risk-free. The bank still needs to work on improving its efficiency and keeping up with strong competition from private players.

If you’re someone who is thinking long term and can handle a bit of uncertainty, this stock might be worth considering. But it’s important to stay patient and keep an eye on how the bank continues to perform over time.

At the end of the day, treat this as just one part of your research. Take your time, understand your own risk level, and invest only when you feel confident about your decision.

Related Posts :

Share This Post